Fixed-rate mortgages offer payment stability and protection against rising rates — ideal if you're staying 7+ years. Adjustable-rate mortgages (ARMs) give lower initial payments but carry adjustment risk — best if you plan to sell or refinance within 3–7 years. Run your numbers through a mortgage calculator before deciding.

When buying a home, few decisions carry as much financial weight as choosing between a fixed vs adjustable rate mortgage. Get it right, and you could save tens of thousands of dollars. Get it wrong, and you could face payment shock that strains your budget for years.

Most homebuyers focus on the interest rate number alone. But the fixed vs adjustable rate mortgage decision involves much more: your time horizon, risk tolerance, the rate environment, and how each loan type affects your monthly budget and long-term equity. Here's everything you need to make the right call.

What Is a Fixed-Rate Mortgage?

A fixed-rate mortgage locks in your interest rate for the entire life of the loan. Your monthly principal and interest payment never changes — whether that's 15, 20, or 30 years later.

How the rate works: Your rate is set at closing based on market conditions and your credit profile. It doesn't move with inflation, Federal Reserve decisions, or economic shifts. For the full loan term, you're completely protected from rising rates.

Most common fixed-rate terms

- 30-year fixed: Lower monthly payment, higher total interest paid over the life of the loan

- 15-year fixed: Higher monthly payment, but dramatically lower total interest

- 20-year fixed: A middle ground between the two — shorter than 30-year, lower payment than 15-year

You pay a premium for certainty. Fixed rates are typically higher than initial ARM rates because the lender takes on the risk that market rates will rise over the next 30 years — and prices that risk into your rate.

What Is an Adjustable-Rate Mortgage (ARM)?

An ARM has an interest rate that stays fixed for an initial period — then adjusts periodically based on a market index. After the fixed period ends, your rate can go up, down, or stay the same at each adjustment interval.

How the rate works: ARMs are structured with two key numbers. A "5/1 ARM" means the rate is fixed for 5 years, then adjusts annually. A "7/1 ARM" fixes for 7 years, then adjusts annually. A "10/1 ARM" fixes for 10 years.

The three components of every ARM

- Index: The benchmark rate your ARM follows. Most ARMs today use SOFR (Secured Overnight Financing Rate), which replaced LIBOR in 2023.

- Margin: A fixed percentage added to the index, typically 2.0–2.75%. This stays the same for the entire loan term.

- Caps: Limits on rate increases — initial cap (first adjustment), periodic cap (each subsequent adjustment), and lifetime cap (total increase over the loan).

Common ARM types

| ARM Type | Fixed Period | Adjustment Frequency | Best For |

|---|---|---|---|

| 5/1 ARM | 5 years | Annually | Homeowners staying 3–6 years |

| 7/1 ARM | 7 years | Annually | Homeowners staying 5–9 years |

| 10/1 ARM | 10 years | Annually | Homeowners staying 8–12 years |

| 5/6 ARM | 5 years | Every 6 months | Short-term owners who expect rates to fall |

You get a lower initial rate — often 0.5–1% below a comparable fixed-rate mortgage. In exchange, you accept the risk that your rate could rise after the initial fixed period ends.

Fixed vs Adjustable Rate Mortgage: Full Comparison

Here's how the two loan types compare across every dimension that matters for your decision:

| Factor | Fixed-Rate Mortgage | Adjustable-Rate Mortgage (ARM) |

|---|---|---|

| Rate certainty | Guaranteed for full loan term | Fixed only during initial period, then variable |

| Initial payment | Higher than ARM at current rates | Lower by ~0.5–1.0% |

| Long-term cost | Predictable from day one | Unknown — depends on future rate movements |

| Payment stability | Completely stable throughout | Stable initially, changes at each adjustment |

| Rate risk | None — fully protected from rising rates | Rate can rise substantially after fixed period |

| Rate protection | Full protection for entire loan term | Caps limit — but do not eliminate — increases |

| Best for | Long-term owners who value stability | Short-term owners planning to sell or refinance |

| Worst-case scenario | Slightly higher payment if rates fall | Payment jumps significantly at adjustment |

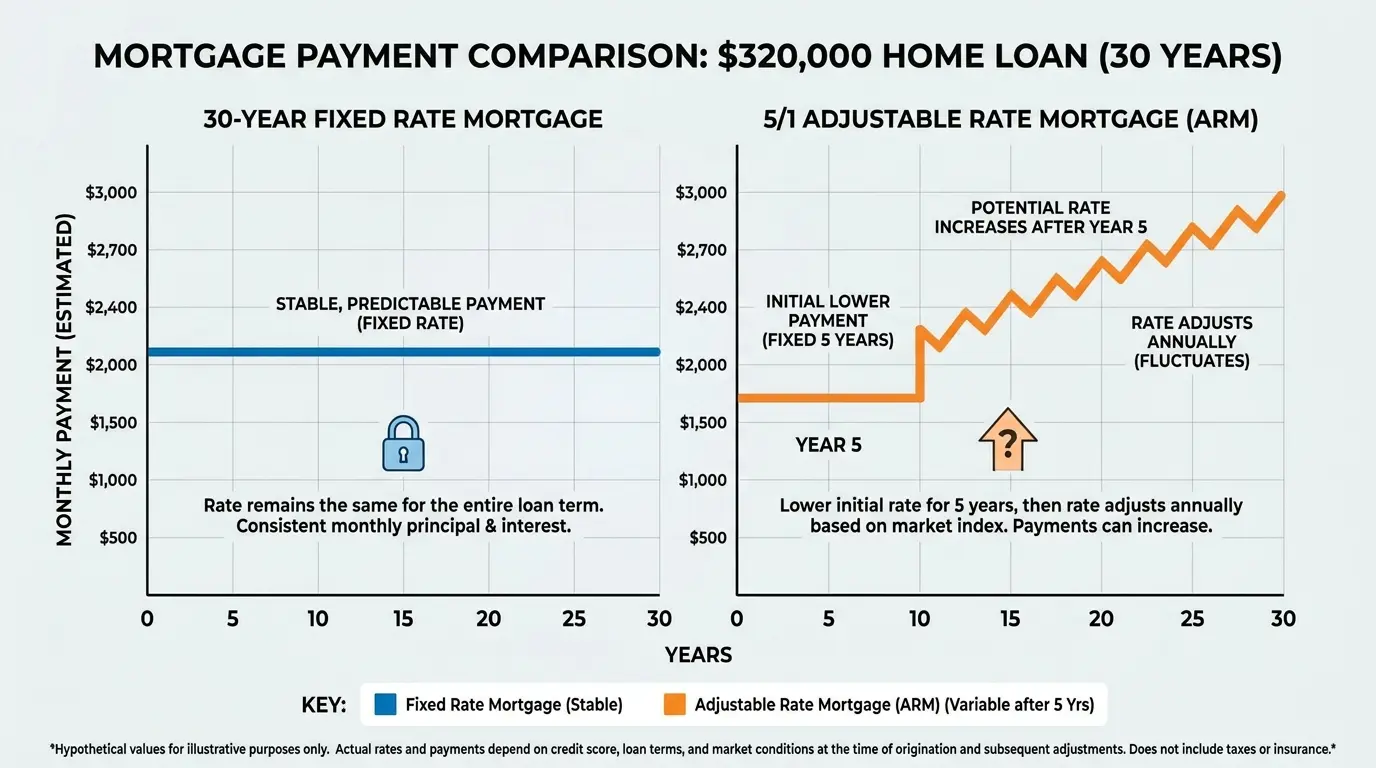

Real-World Payment Examples: Fixed vs ARM on the Same Loan

To understand the true difference, let's use concrete numbers on the same loan amount. Compare a 30-year fixed at 6.75% against a 5/1 ARM at 6.25% — a realistic spread of 0.5 percentage points on a $320,000 loan (20% down on a $400,000 home).

| Loan Type | Rate | Monthly P&I | Total Paid (5 yrs) | Balance After 5 yrs | Interest Paid (5 yrs) |

|---|---|---|---|---|---|

| 30-Year Fixed | 6.75% | $2,076 | $124,560 | $300,040 | ~$99,600 |

| 5/1 ARM | 6.25% | $1,970 | $118,200 | $299,380 | ~$93,500 |

| ARM Advantage | — | −$106/mo | −$6,360 | $660 more equity | ~$6,100 less interest |

If you sell or refinance before year 6, the ARM wins clearly — $6,100 less interest and $660 more equity for doing nothing more than choosing the right loan structure.

What happens when the ARM adjusts in year 6?

The 5/1 ARM rate becomes index + margin. Suppose SOFR has risen to 5.0% by year 6:

- New rate = 5.0% + 2.25% margin = 7.25%

- With a 2% initial cap, the rate can only jump to 8.25% maximum at first adjustment

- New payment on remaining $299,380 balance over 25 years: ~$2,175/month

- Payment increase: +$205/month compared to staying in the fixed-rate loan

"The ARM saves $106/month for the first 5 years. Then in year 6, in a rising-rate environment, you could pay $205/month more than if you'd chosen the fixed rate. Time horizon is everything."

When Fixed-Rate Mortgages Win

- Plan to stay 7+ years

- Value payment certainty above all

- Have a fixed income or tight budget

- Are buying in a rising-rate environment

- Don't want to think about rates for 30 years

- Plan to sell or refinance in 3–7 years

- Expect rates to stay flat or fall

- Have strong savings to absorb a payment increase

- Plan to pay off the loan aggressively

- The fixed/ARM rate spread is unusually wide (1%+)

The long-term math on staying 10+ years

On a $320,000 loan, every 1% rate increase costs about $200 more per month. If you're in year 10 of a 30-year fixed at 6.75% and market rates have risen to 9%, you're saving roughly $2,400 per year compared to what you'd pay on a new loan. Over the remaining 20 years, that protection is worth more than the lower initial rate the ARM offered.

When an ARM is clearly the right call

A young professional buying a condo they'll sell in 5 years saves $106/month — over $6,000 total — with no adjustment risk, because they'll close or refinance before the first adjustment. The ARM's lower rate is pure savings with no downside.

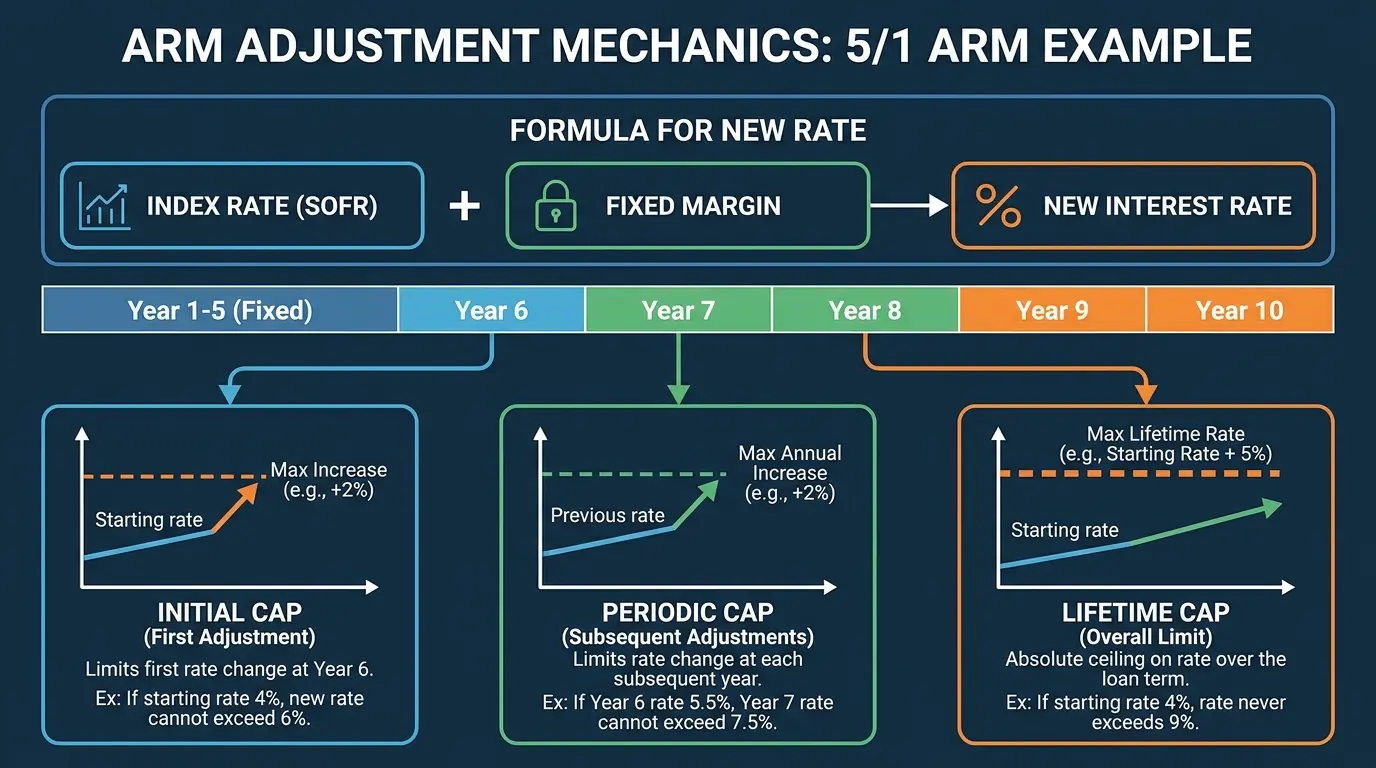

Understanding ARM Adjustments: The Mechanics

If you're considering an ARM, you need to understand exactly how adjustments work — because that's where the risk lives.

The index

Most ARMs today use the Secured Overnight Financing Rate (SOFR), which replaced LIBOR in 2023. SOFR reflects overnight borrowing costs between financial institutions and is considered more stable and transparent than its predecessor. Other ARM indexes you may encounter: Constant Maturity Treasury (CMT), Prime Rate, and 11th District Cost of Funds Index (COFI).

The margin

Your margin is added to the index to determine your fully indexed rate. It's fixed for the life of the loan — typically 2.0%–2.75%. If your margin is 2.25% and the index is 4.0%, your rate is 6.25%.

Rate caps: your protection against huge increases

| Cap Type | Typical Limit | What It Means |

|---|---|---|

| Initial cap | 2% | Rate can't increase more than 2% at the first adjustment |

| Periodic cap | 2% | Rate can't increase more than 2% at each subsequent adjustment |

| Lifetime cap | 5% | Rate can't increase more than 5% above the initial rate over the entire loan |

Worst-case scenario: 5/1 ARM at 6.25%

Always run a worst-case scenario before choosing an ARM. Assume the rate increases by the maximum allowed at every adjustment:

| Year | Rate | Monthly Payment | Change vs. Fixed ($2,076) |

|---|---|---|---|

| 1–5 | 6.25% | $1,970 | −$106/mo |

| 6 | 8.25% (2% initial cap) | $2,218 | +$142/mo |

| 7 | 10.25% (2% periodic cap) | $2,541 | +$465/mo |

| 8+ | 11.25% (lifetime cap hit) | $2,780 | +$704/mo |

In the worst case, the payment rises from $1,970 to $2,780 — an increase of $810/month (41%). If that level would cause financial hardship, a fixed-rate mortgage is the correct choice regardless of the initial rate savings.

Lenders are legally required (per CFPB rules) to show you the maximum possible payment under your ARM. Ask for this disclosure and use it as your stress test — not just the initial rate.

Enter your home price, down payment, and both rates — see monthly payment difference, total interest, and break-even year side by side.

How to Choose: A Step-by-Step Framework

Step 1: Determine your likely time horizon

| Time in Home | Recommended Loan Type | Why |

|---|---|---|

| 1–3 years | 5/1 or 7/1 ARM | Out before any adjustment — rate savings with no risk |

| 3–5 years | ARM is competitive | Compare total cost including expected adjustment scenarios |

| 5–7 years | Either — run the numbers | Break-even analysis determines the winner |

| 7–10+ years | Fixed-rate mortgage | Rate protection value outweighs ARM's initial savings |

Step 2: Assess your risk tolerance

- Can you absorb a 20–30% increase in your monthly mortgage payment without financial stress?

- Do you have an emergency fund covering 3–6 months of expenses?

- Is your income stable and likely to grow — or fixed?

If payment uncertainty would cause anxiety or budget strain, the fixed-rate mortgage is worth the rate premium. Peace of mind has real financial value.

Step 3: Evaluate the current rate environment

Are mortgage rates historically high or low? What's the Federal Reserve's current policy direction? No one can predict rates with certainty, but understanding the broader environment helps you assess whether ARM adjustment risk is worth taking. In rising-rate environments, fixed rates become more attractive. In flat or falling environments, ARMs become more competitive.

Step 4: Calculate the break-even point

Use a mortgage calculator to find the year at which the fixed-rate mortgage becomes cheaper than the ARM (accounting for expected adjustments). If you plan to sell before that break-even year, the ARM wins. If you plan to stay past it, the fixed rate wins.

The Hybrid Solution: 7/1 and 10/1 ARMs

If a 5/1 ARM seems too short and a 30-year fixed seems too expensive, the 7/1 or 10/1 ARM offers a middle ground that many homeowners overlook.

| ARM Type | Fixed Period | Rate vs 30-Year Fixed | Best For |

|---|---|---|---|

| 7/1 ARM | 7 years | ~0.4–0.6% lower | Homeowners staying 5–9 years — more stability than 5/1 |

| 10/1 ARM | 10 years | ~0.2–0.4% lower | Homeowners staying 8–12 years — significant first-decade savings |

For most homeowners who aren't sure of their timeline, the 7/1 ARM offers the best balance: 7 years of payment stability, enough time to build equity and plan ahead, with a lower initial rate than the 30-year fixed. By year 7, you may be ready to sell, refinance, or have sufficiently grown your income to absorb a potential adjustment.

5 Common Mistakes When Choosing Between Fixed and ARM

Mistake 1: Not understanding adjustment mechanics. Many borrowers sign up for an ARM without fully understanding their loan's index, margin, or cap structure. Always read the ARM disclosure document (CHARM booklet) and ask questions before signing.

Mistake 2: Overestimating how long they'll stay. A surprising number of homeowners expect to stay 10 years but move in year 7 due to life changes — job relocation, growing family, divorce. If you choose a fixed rate based on a long-term stay that doesn't materialize, you paid a higher rate unnecessarily. If you choose an ARM expecting to leave in 5 years but stay 8, you face adjustment risk you didn't plan for.

Mistake 3: Ignoring the rate spread. When the difference between fixed and ARM rates narrows to 0.25%–0.375%, the ARM becomes far less attractive. In that environment, the fixed rate is often the better deal even for moderate-length stays.

Mistake 4: No plan for adjustment. The most successful ARM borrowers have a clear strategy before adjustment approaches — sell, refinance into a fixed rate, or prepare for a higher payment. Without a plan, the adjustment catches borrowers off guard.

Mistake 5: Forgetting refinance costs. ARM borrowers who plan to refinance before adjustment need to account for closing costs of 2–5% of the loan amount. On a $320,000 loan, that's $6,400–$16,000. If you refinance twice over a 10-year period, those costs can easily consume the savings from the ARM's lower initial rate.

Frequently Asked Questions

Conclusion: Making Your Fixed vs Adjustable Rate Mortgage Decision

Choosing between a fixed vs adjustable rate mortgage comes down to three things: how long you plan to stay, how much payment risk you can absorb, and what the numbers actually show for your specific loan.

- Fixed-rate mortgages offer certainty and full rate protection. You never worry about payment increases. The cost is a higher initial rate compared to an ARM.

- ARMs offer lower initial rates — typically 0.5–1% less. The cost is uncertainty: your rate and payment can rise substantially after the fixed period ends.

- Your time horizon matters most. Staying 5 years or less? An ARM often wins. Staying 10+ years? A fixed rate is usually the right call.

- Always run the worst case. Know your index, margin, and caps. Make sure the maximum possible ARM payment is one you can absorb before you sign.

- Have a plan. If you choose an ARM, decide in advance what you'll do as the adjustment approaches — refinance, sell, or prepare for the higher payment.

CalcMeter's free mortgage calculator shows fixed vs ARM monthly payment comparison, total interest, break-even year, and full amortization schedule. No sign-up needed.