Most first-time buyers focus on the interest rate and the monthly payment number. That is a reasonable starting point, but it misses a great deal. Your monthly payment is made up of four distinct components. The split between principal and interest shifts dramatically over time. PMI adds hundreds per year — and has an exact cancellation date. And a modest extra payment made early enough can cut years off your loan and save more than a car's worth of interest.

This guide walks through each piece of the mortgage payment, the formula behind it, and the decisions that actually move the number in your favour.

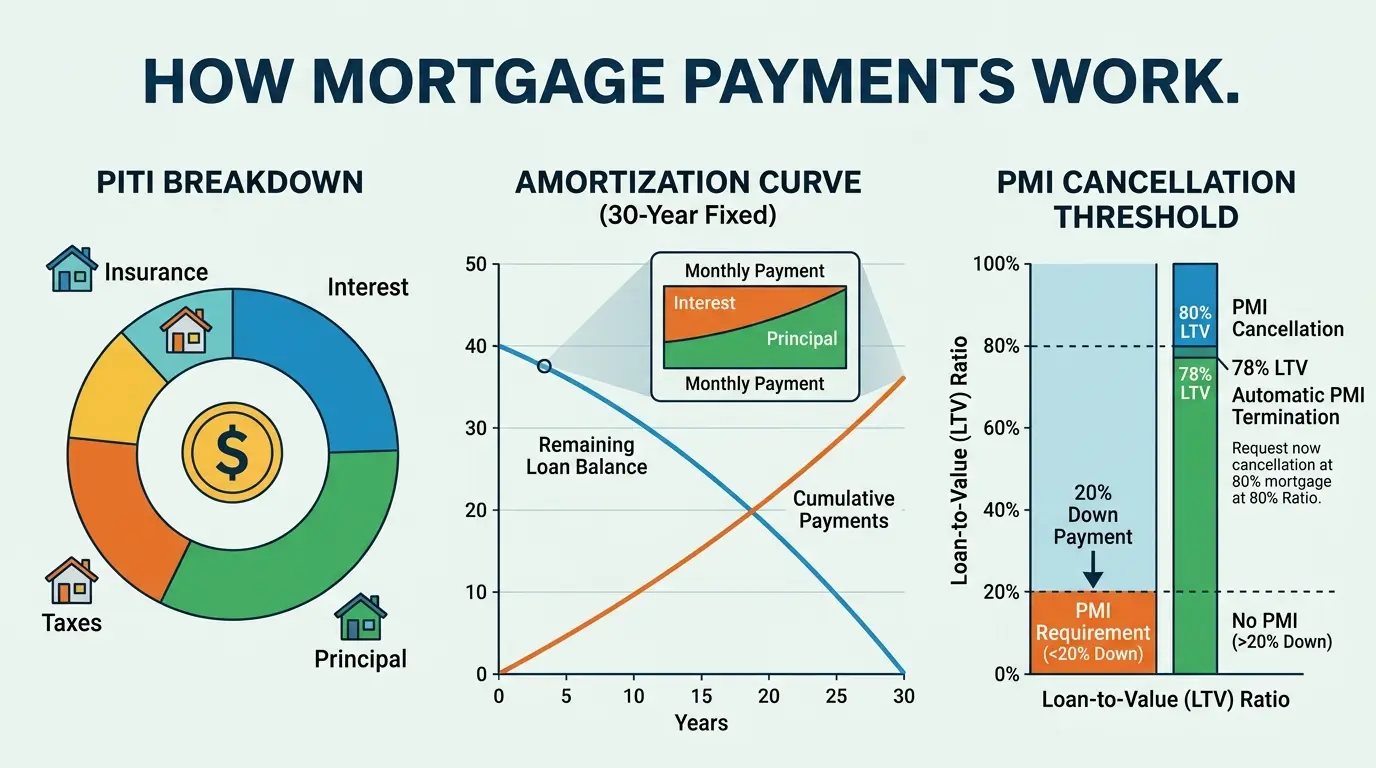

What Is PITI? The Four Parts of Every Mortgage Payment

When your lender tells you the monthly payment, they typically mean the full PITI amount — not just principal and interest. PITI stands for Principal, Interest, Taxes, and Insurance. Each serves a different purpose, and each can be adjusted independently.

Most lenders collect property tax and homeowner's insurance monthly, hold the funds in an escrow account, and pay the bills on your behalf when they come due. This means your "mortgage payment" includes more than the bank technically needs — it's a bundled payment covering your full housing cost obligation.

The Mortgage Payment Formula (And What the Numbers Actually Mean)

The principal and interest portion of your payment is calculated using a fixed-rate amortization formula. This produces a payment that stays constant for the life of the loan, even though the internal split between principal and interest changes every month.

$320,000 loan at 7% for 30 years:

r = 0.07 ÷ 12 = 0.005833 | n = 30 × 12 = 360

M = 320,000 × [0.005833 × (1.005833)^360] ÷ [(1.005833)^360 − 1]

M = 320,000 × [0.005833 × 8.117] ÷ [8.117 − 1] = 320,000 × 0.04735 ÷ 7.117 = $2,129/month

Your full monthly payment adds property tax, homeowner's insurance, and PMI on top of the P&I. On that same $320,000 loan, with $4,800/year in property tax ($400/mo), $1,200/year insurance ($100/mo), and PMI at 0.5% of the loan ($133/mo), the total PITI payment becomes roughly $2,762/month.

Why the interest rate matters more than most buyers realise

A 1% difference in rate does not feel significant. Over 30 years on a $300,000 loan, it is the difference between paying $280,000 and $418,000 in total interest — a gap of $138,000.

| Interest Rate | Monthly P&I ($300k loan) | Total Interest Paid | Total Cost |

|---|---|---|---|

| 5.0% | $1,610 | $279,767 | $579,767 |

| 6.0% | $1,799 | $347,515 | $647,515 |

| 7.0% | $1,996 | $418,527 | $718,527 |

| 8.0% | $2,201 | $492,311 | $792,311 |

Enter your home price, down payment, rate, and term — get your full PITI breakdown with PMI removal date and amortization schedule. Free, no sign-up.

How Mortgage Amortization Works

Amortization is the process of paying off a loan through scheduled payments over time. What makes a mortgage unusual is that each payment is the same size, but the split inside it changes with every passing month.

In month 1 of a $320,000 loan at 7%, interest is charged on the full balance: $320,000 × 0.005833 = $1,867 in interest. The remaining $262 of your $2,129 payment reduces your balance. In month 2, your balance is $319,738, so the interest charge drops slightly — meaning a slightly larger slice of the same payment goes to principal. This process repeats for 360 months.

"In the first year of a 30-year mortgage at 7%, roughly 88 cents of every dollar you pay goes to interest, not your home equity."

| Year | Principal Paid (year) | Interest Paid (year) | Remaining Balance |

|---|---|---|---|

| 1 | $3,234 | $22,314 | $316,766 |

| 5 | $4,285 | $21,263 | $301,235 |

| 10 | $6,090 | $19,458 | $274,621 |

| 15 | $8,608 | $16,940 | $236,909 |

| 20 | $12,172 | $13,376 | $183,434 |

| 25 | $17,398 | $8,150 | $107,514 |

| 30 | $24,678 | $870 | $0 |

Based on a $320,000 loan at 7% for 30 years with a base P&I payment of $2,129/month.

When does the split flip in your favour?

On a 30-year mortgage at 7%, the crossover point — where more of each payment goes to principal than to interest — happens around month 222 (year 18.5). That is a long time to wait. This is the core reason extra payments made in the early years are so disproportionately powerful: each extra dollar of principal you pay in year 2 saves 28 years of compounding interest charges on that dollar.

What Is PMI and Exactly When Does It Go Away?

PMI — Private Mortgage Insurance — is a monthly premium charged to borrowers who put down less than 20% of the home price. It protects the lender, not you, in the event of default. PMI typically costs 0.2%–1.5% of the loan amount per year, with 0.5% being a common midpoint for borrowers with good credit.

| Loan Amount | PMI at 0.5%/yr | Monthly Cost | Annual Cost |

|---|---|---|---|

| $200,000 | $1,000/yr | $83 | $1,000 |

| $280,000 | $1,400/yr | $117 | $1,400 |

| $320,000 | $1,600/yr | $133 | $1,600 |

| $400,000 | $2,000/yr | $167 | $2,000 |

| $500,000 | $2,500/yr | $208 | $2,500 |

Under the Homeowners Protection Act (HPA), your lender must automatically cancel PMI on the date your loan balance is scheduled to reach 80% of the original home value — you don't need to ask. PMI must also be terminated when your balance reaches 78% of the original value, even if you haven't requested it.

On a $400,000 home with 10% down ($360,000 loan) at 7%, PMI cancels automatically around month 96 (year 8) when the scheduled balance hits $320,000. Our mortgage calculator shows you this exact date based on your specific inputs.

If your home's market value has risen since purchase, you may be able to prove 20% equity with a new appraisal before the scheduled cancellation date. Contact your loan servicer with a written request — they are required to respond. This option is not automatic; you must initiate it.

15-Year vs. 30-Year Mortgage — The Real Numbers

The 15-year vs. 30-year decision is one of the most consequential financial choices in a mortgage. The difference in total cost is enormous — but so is the difference in monthly cash flow.

| 30-Year @ 7.0% | 15-Year @ 6.4% | Difference | |

|---|---|---|---|

| Loan Amount | $320,000 | $320,000 | — |

| Monthly P&I | $2,129 | $2,770 | +$641/mo |

| Total Interest | $446,440 | $178,600 | Save $267,840 |

| Total Cost | $766,440 | $498,600 | Save $267,840 |

| Payoff Date | 30 years | 15 years | 15 years sooner |

The 15-year saves $267,840 in interest — roughly the cost of a second home. But the monthly payment is $641 higher. The honest case for the 30-year: if you invest that $641/month difference in a broad index fund at 8% annual return over 30 years, you accumulate approximately $913,000 — likely exceeding the interest saved on the 15-year.

Take a 30-year mortgage for the flexibility of lower required payments, but make voluntary extra payments to shorten the effective term. You get the safety net of a lower minimum payment without paying 30 years of interest.

The 15 vs 30 Year tab on CalcMeter's mortgage calculator shows your exact monthly difference, interest saved, and break-even return rate — instantly.

How Extra Payments Cut Years Off Your Loan

Every dollar of extra principal payment immediately reduces the balance on which future interest is charged. The effect compounds — a $200 extra payment in month 1 saves interest in every one of the remaining 359 months. That compounding is why the total savings are so much larger than the extra amount paid.

| Extra Monthly Payment | New Payoff | Years Saved | Interest Saved |

|---|---|---|---|

| $0 (base) | 30 years | — | — |

| +$100/month | ~26 years | 4 years | ~$71,000 |

| +$200/month | ~23 years | 7 years | ~$119,000 |

| +$500/month | ~17.7 years | 12.3 years | ~$209,000 |

Based on a $320,000 loan at 7% for 30 years. Extra payments applied to principal each month.

The lump-sum extra payment

A one-time extra payment — a tax refund, annual bonus, or inheritance — applied directly to mortgage principal works on the same principle. A $5,000 lump-sum payment in year 2 of a $320,000 loan at 7% saves approximately $22,000 in interest over the loan's life and cuts about 14 months off the payoff date.

Instruct your lender in writing to apply any extra payment to principal only, not to advance your next scheduled payment date. Some servicers will credit the extra amount as a future payment by default, which does not reduce your principal balance at all. Check your statement after the first extra payment to confirm it was applied correctly.

How to Lower Your Monthly Mortgage Payment

If your current or planned payment feels too high, there are five legitimate levers:

- Increase your down payment. A larger down payment reduces the loan amount, lowers monthly P&I, and may eliminate PMI entirely. Going from 10% to 20% down on a $400,000 home saves roughly $133/month in PMI alone, plus reduces the P&I on a smaller loan.

- Improve your credit score before applying. A score above 740 typically qualifies for the best available rates. Moving from a 680 to a 740 score can reduce your rate by 0.25%–0.5%, saving $40–$80/month on a $300,000 loan.

- Extend the loan term. A 30-year mortgage has a lower required monthly payment than a 15-year on the same balance. You pay more total interest, but the monthly obligation is lower. The voluntary extra payments strategy (above) lets you get the best of both.

- Buy mortgage points. Paying 1% of the loan amount upfront (one "point") typically reduces the rate by 0.25%. On a $320,000 loan, one point costs $3,200 and saves about $53/month — the break-even is 5 years. Only worthwhile if you stay in the home past that point.

- Refinance when rates drop. If market rates fall 0.75% or more below your current rate, refinancing often makes financial sense — depending on closing costs and how long you plan to stay. Calculate the break-even period (closing costs ÷ monthly savings) before committing.

How to Calculate Mortgage Affordability

Lenders use two ratios — the front-end ratio and the back-end ratio — to determine how much mortgage they'll approve. These same ratios are the most reliable way to assess affordability before you start house hunting.

The standard is the 28/36 rule:

- Front-end ratio (28%): Your total monthly housing payment (PITI) should not exceed 28% of your gross monthly income.

- Back-end ratio (36%): Your total monthly debt obligations — mortgage plus car loans, student loans, and credit card minimums — should not exceed 36% of gross income.

| Annual Salary | Gross Monthly Income | Max Housing Payment (28%) | Max Total Debt (36%) |

|---|---|---|---|

| $60,000 | $5,000 | $1,400 | $1,800 |

| $80,000 | $6,667 | $1,867 | $2,400 |

| $100,000 | $8,333 | $2,333 | $3,000 |

| $120,000 | $10,000 | $2,800 | $3,600 |

| $150,000 | $12,500 | $3,500 | $4,500 |

These are maximum thresholds, not targets. Many financial planners recommend keeping housing costs at 25% or below — leaving more room for savings, emergencies, and other financial goals. The 28% limit also needs to cover taxes, insurance, PMI, and HOA fees — not just P&I — so the actual loan amount it supports is significantly lower than the headline number suggests.

CalcMeter's Affordability tab applies the 28/36 rule to your salary, debts, and down payment — showing three scenarios (conservative, moderate, aggressive) instantly.

Frequently Asked Questions

CalcMeter's free mortgage calculator covers monthly payment, affordability, extra payments, 15 vs 30 year comparison, and a full amortization schedule — formula shown for every result.