Albert Einstein reportedly called compound interest the eighth wonder of the world. Whether he actually said it is debated — but the math is not. Given enough time, compound interest turns ordinary monthly contributions into extraordinary wealth. The challenge is that it looks painfully slow in the early years, which is exactly when most people give up.

This guide explains how compound interest actually works, why the monthly vs lump sum debate matters (and which one usually wins), how to use the Rule of 72 as a mental shortcut, and what practical steps maximize your returns. All with real numbers, not motivational platitudes.

Try it yourself: The CalcMeter Investment Calculator calculates your exact portfolio value, year-by-year growth breakdown, and lump sum vs monthly comparison — free, instant, no signup.

How Compound Interest Actually Works

Simple interest pays you a fixed return on your original principal only. You deposit $10,000 at 10% simple interest — you earn $1,000 every year, forever. After 30 years: $10,000 + ($1,000 × 30) = $40,000.

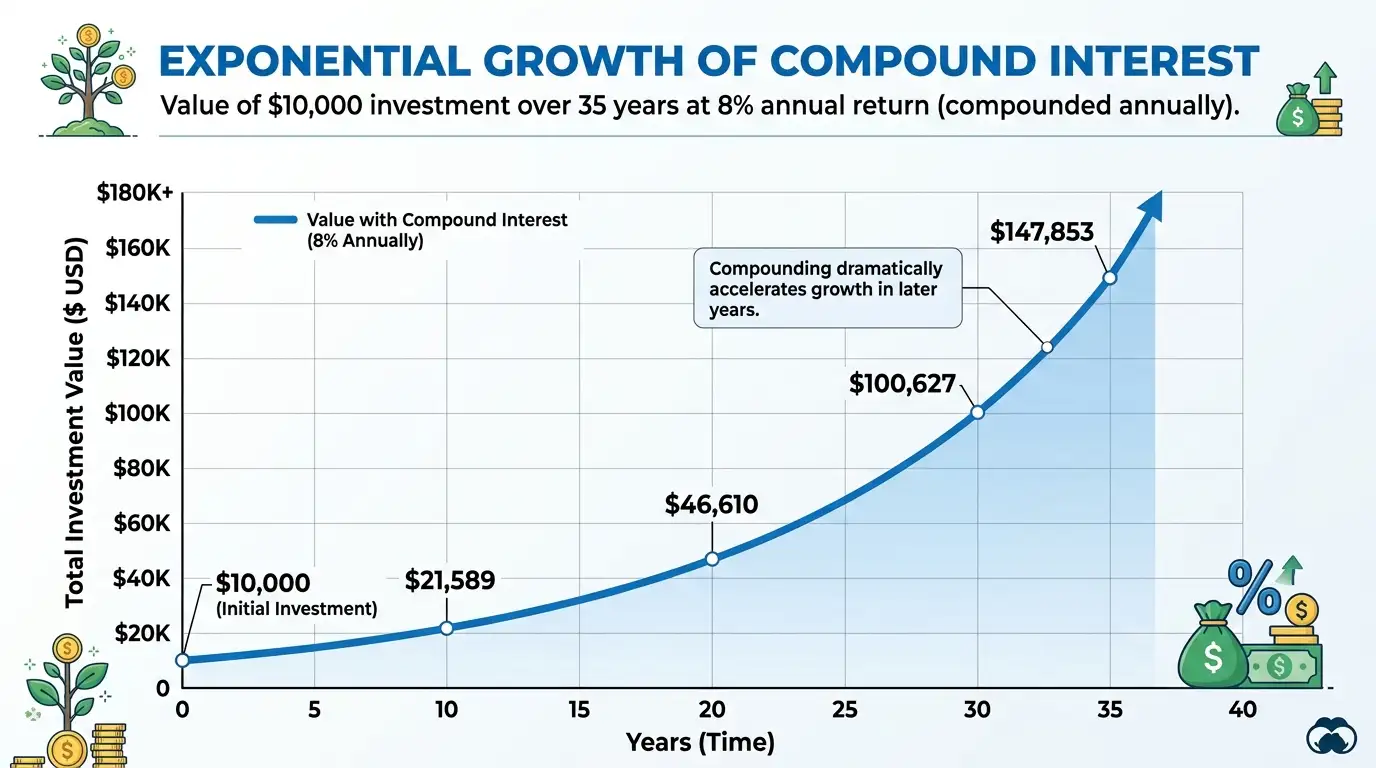

Compound interest is fundamentally different. In Year 1, you earn 10% on $10,000 = $1,000. In Year 2, you earn 10% on $11,000 = $1,100. In Year 3, 10% on $12,100 = $1,210. The interest keeps earning interest. After 30 years, that same $10,000 at 10% compound interest grows to $174,494 — more than four times the simple interest result.

The variable that matters most is not the rate — it's time. Here's the same $10,000 at 10% compounded annually across different horizons:

| Duration | Starting Amount | Final Value | Total Gain |

|---|---|---|---|

| 10 years | $10,000 | $25,937 | +$15,937 |

| 20 years | $10,000 | $67,275 | +$57,275 |

| 30 years | $10,000 | $174,494 | +$164,494 |

| 40 years | $10,000 | $452,593 | +$442,593 |

Notice what happens between Year 20 and Year 30: the portfolio grows by $107,219. Between Year 30 and Year 40 it grows by $278,099. The same 10 years produces 2.6× more wealth simply because the base is larger. This is the acceleration effect of compounding — and it's why starting early is the single most impactful financial decision most people can make.

The 5-year cost of waiting: A 25-year-old who invests $400/month at 10% will have approximately $2.7 million by age 65. A 30-year-old doing the exact same thing ends up with about $1.5 million — $1.2 million less, purely from waiting 5 years to start.

The Investment Return Formula, Explained

There are two formulas you need — one for a single lump sum, and one for regular monthly contributions. Both use compound interest, but the monthly version accounts for the fact that each payment compounds for a different length of time.

Lump Sum Formula

When you invest a single amount and leave it alone, the math is straightforward:

Example: $10,000 at 10% for 20 years

FV = 10,000 × (1.10)²⁰ = $67,275

r = Annual return rate ÷ 100

n = Number of years

Monthly Contribution Formula (Annuity)

When you invest a fixed amount every month, the formula accounts for each payment compounding individually. Your first payment has the most time to grow; your last payment barely compounds at all:

Example: $500/mo at 10% for 20 years

r = 10 ÷ 12 ÷ 100 = 0.00833, n = 240 months

FV = $382,697

r = Monthly rate = Annual% ÷ 12 ÷ 100

n = Total months = Years × 12

In the monthly example: you contribute $500 × 240 months = $120,000 total. Your portfolio grows to $382,697. That's $262,697 in pure investment gains — more than double what you put in — generated entirely by compound growth on a very modest monthly contribution.

Run your own numbers instantly

Enter your monthly amount, duration, and expected return rate — get your exact portfolio value, year-by-year breakdown, and lump sum comparison in seconds.

Open Investment CalculatorMonthly Investing vs Lump Sum: Which Wins?

This is one of the most-searched personal finance questions — and it has a clear, research-backed answer that most people get wrong.

A Vanguard study analyzing 58 years of US market data (as well as UK and Australian markets) found that lump sum investing outperforms dollar-cost averaging (monthly investing) approximately two-thirds of the time. The reason is structural: when you deploy all your money at once, 100% of it is compounding from day one. Monthly investing means your early payments compound well, but late payments barely compound at all.

Here's the same $120,000 deployed two ways at 10% over 20 years:

| Strategy | Amount Deployed | Final Value | Verdict |

|---|---|---|---|

| Lump Sum ($120K upfront) | $120,000 on day one | $806,231 | Wins 2/3 of the time |

| Monthly ($500/mo × 240) | $120,000 over 20 years | $382,697 | Practical for most people |

Lump sum generates more than twice the final value here — because the entire $120,000 compounds for 20 years, while monthly contributions average only 10 years of compounding.

So should everyone invest as a lump sum? Not necessarily. Three important caveats:

- Most people don't have $120,000 sitting idle. Salaried workers build wealth gradually — monthly investing is not a suboptimal choice, it's the only realistic one for most households.

- Lump sum at a market peak is painful. If you invest everything right before a 40% market correction, you're watching a large sum shrink dramatically. Monthly investing smooths this out — you buy cheaper during the dip and recover faster.

- Monthly investing wins in bear markets. During sustained downturns, dollar-cost averaging accumulates more shares at lower prices, setting up stronger recovery gains. Lump sum investors who entered at the peak of 2000 or 2007 underperformed DCA investors for years.

Practical rule: If you have a windfall — bonus, tax refund, inheritance — deploy it as a lump sum into a broad index fund. Don't spread it out trying to time the market. The math favors immediate deployment in the majority of scenarios.

The Rule of 72: Quick Mental Math for Investors

The Rule of 72 is the most useful mental math shortcut in personal finance. It answers one question instantly: how long does it take to double my money?

Divide 72 by your annual return rate. The result is roughly how many years until your investment doubles.

| Annual Return | Years to Double (Rule of 72) | Actual Years | Example |

|---|---|---|---|

| 4% (High-yield savings) | 18 years | 17.7 years | $10K → $20K by 2044 |

| 6% (Conservative portfolio) | 12 years | 11.9 years | $10K → $20K by 2038 |

| 7% (Bonds + equities) | 10.3 years | 10.2 years | $10K → $20K by 2036 |

| 10% (S&P 500 avg) | 7.2 years | 7.3 years | $10K → $20K by 2033 |

| 12% (Growth stocks) | 6 years | 6.1 years | $10K → $20K by 2032 |

The Rule of 72 also works in reverse for inflation. At 3% inflation, your money's purchasing power halves in 24 years (72 ÷ 3). This is why keeping money in a 0.5% savings account is a guaranteed loss in real terms — your cash loses purchasing power faster than it gains interest.

At 10% return, a portfolio doubles every 7.2 years. Starting at $10,000 at age 25: $20K by 32 → $40K by 39 → $80K by 46 → $160K by 53 → $320K by 60 → $640K by 67. No additional contributions, just compound growth on the original $10,000.

How to Maximize Your Investment Returns

The math of compound interest is fixed — you can't change the formula. But you can control the inputs that determine your outcome: time, contribution amount, return rate, and costs.

1. Start as Early as Possible

The single most powerful lever is time. Every year you delay costs you approximately one doubling cycle at the end of your investment horizon. A 25-year-old investor contributes the same $500/month as a 30-year-old but ends up with roughly 80% more wealth — not because they invested more, but because their money had 5 more years to compound.

2. Max Your Tax-Advantaged Accounts First

The order in which you invest matters almost as much as how much you invest. Standard priority for US investors:

- 1Contribute to your 401(k) up to the employer match — this is an instant 50–100% return with zero market risk.

- 2Max your Roth IRA ($7,000/year in 2026 if under 50). All growth is permanently tax-free.

- 3Return to 401(k) and contribute up to the annual maximum ($23,500 in 2026).

- 4Invest remaining funds in a taxable brokerage account focused on tax-efficient index funds.

3. Minimize Expense Ratios

Expense ratios are annual fees charged by mutual funds and ETFs, expressed as a percentage of your assets. They compound against you — a 1% fee vs. 0.05% (e.g., Vanguard VTSAX or Fidelity ZERO funds) can cost you over $100,000 on a $500K portfolio over 20 years. Broad market index funds consistently beat actively managed funds after fees over 15+ year periods.

4. Never Stop During Downturns

The worst thing a monthly investor can do is pause contributions during a market crash — which is exactly when they should be investing more. During the 2008–2009 financial crisis and the 2020 COVID crash, investors who continued their monthly contributions bought shares at massive discounts and captured the full recovery. Those who paused or sold locked in losses and missed the rebound.

5. Increase Contributions Annually

As your salary grows, increase your monthly investment. Even raising your contribution by $50–$100 per year — aligned with raises — can add tens of thousands to your final portfolio. This "step-up" strategy compounds on itself: more principal means more compounding means faster growth.

Frequently Asked Questions

Compound interest means your returns earn their own returns. In Year 1, you earn interest on your principal. In Year 2, you earn interest on your principal plus Year 1's gains. This snowball grows slowly at first, then accelerates dramatically. A $10,000 investment at 10% over 30 years grows to $174,494 — $164,494 in gains from an initial $10,000 investment, all from compounding.

Vanguard research shows lump sum investing outperforms monthly investing (dollar-cost averaging) about two-thirds of the time in rising markets — because more money compounds from day one. However, monthly investing is the practical reality for most salaried people, eliminates market-timing anxiety, and outperforms lump sum during market downturns. The best strategy is the one you can sustain consistently.

Divide 72 by your annual return rate to estimate how many years it takes to double your money. At 10% return, your investment doubles every 7.2 years. At 7%, every 10.3 years. At 6%, every 12 years. It also works in reverse for inflation: at 3% inflation, your purchasing power halves in 24 years.

At a 10% annual return: $500/month reaches $1 million in about 30 years; $1,000/month in about 24 years; $2,000/month in about 20 years. The earlier you start, the less you need to contribute monthly. Use the CalcMeter Investment Calculator to find your exact number.

Dollar-cost averaging (DCA) means investing a fixed dollar amount at regular intervals regardless of market conditions. When prices fall, your fixed amount buys more shares. When prices rise, it buys fewer. Over time this averages your cost per share and removes the emotional burden of trying to time the market. It's the mechanism behind monthly 401(k) contributions, Roth IRA auto-invest, and automatic brokerage contributions.

The S&P 500 has historically returned approximately 10% per year on average before inflation (about 7% after inflation) over long periods. For conservative planning, most financial planners use 7% to account for inflation. Bond-heavy portfolios average 4–6%. Use 10% for an all-equity index fund scenario, and 7% for a more conservative real-return projection. Past performance does not guarantee future results.