Most people focus on two numbers when they take out a mortgage: the interest rate and the monthly payment. That's a reasonable starting point — but it misses nearly everything important about how a mortgage actually works.

Your monthly payment is fixed for the life of the loan. But what that payment is doing changes completely over time. Early on, the vast majority goes to interest. By the end, almost all of it reduces your balance. The gradual shift between those two outcomes is mortgage amortization — and once you understand it, you'll see your mortgage in an entirely different way.

What Is Mortgage Amortization? (The Simple Version)

The word "amortization" sounds complicated, but the idea is straightforward. Amortization simply means spreading out your loan payments over a fixed period of time. Each month, you pay a set amount. That payment covers two things: the interest your lender charges and a portion of the actual loan balance (called the principal).

The catch — and this is what most borrowers don't realize — is that the split between interest and principal is not equal throughout your loan. It changes every single month.

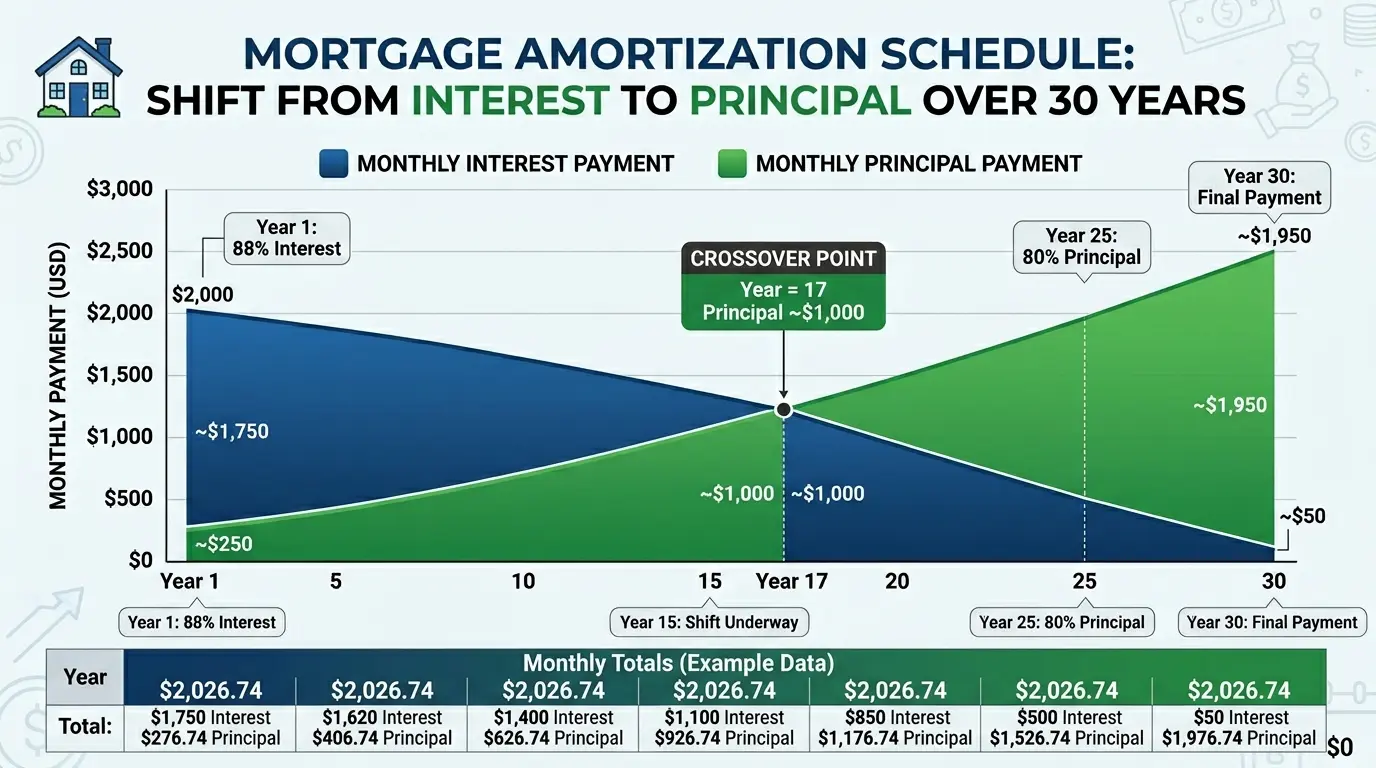

In the early years, you're paying mostly interest. As time goes on, more and more of each payment goes toward the principal. By the final payments of your mortgage, you're barely paying any interest at all — because you've almost paid off the loan.

"Think of amortization like eating a pizza. At the beginning, you're mostly eating the toppings (interest). By the end, you're getting through the thick dough (principal). The slice size stays the same — but the composition changes throughout the meal."

How Does Mortgage Amortization Actually Work?

When you take out a mortgage, your lender calculates your monthly payment using three things:

- The loan amount — how much you borrowed

- The interest rate — what the lender charges you for borrowing

- The loan term — how many years you have to pay it back

Once those three numbers are fixed, your monthly payment stays the same for the life of the loan (assuming a fixed-rate mortgage). But what changes is how that payment is divided between interest and principal. Here's the mechanics:

- Your lender calculates interest based on your remaining loan balance

- That interest amount is deducted from your payment first

- Whatever is left after interest goes toward reducing your principal

- Your new loan balance is slightly lower

- Next month, interest is calculated on that new, lower balance — so slightly less goes to interest and slightly more to principal

This process repeats every single month for the entire life of your loan. It's a slow shift at first, but it accelerates over time.

Example: $250,000 at 6.5% for 30 years

r = 0.065 ÷ 12 = 0.005417 | n = 30 × 12 = 360

M = 250,000 × [0.005417 × (1.005417)^360] ÷ [(1.005417)^360 − 1]

M = $1,580/month

A Real-Life Example to Make This Crystal Clear

Let's walk through a concrete example. You take out a $250,000 home loan at 6.5% interest for 30 years. Your fixed monthly payment is $1,580.

Now let's look at what's actually happening to that $1,580 at different points in the loan:

| Payment | Monthly Payment | Interest Paid | Principal Paid | Remaining Balance |

|---|---|---|---|---|

| Month 1 | $1,580 | $1,354 | $226 | $249,774 |

| Month 60 (Year 5) | $1,580 | $1,286 | $294 | $237,127 |

| Month 120 (Year 10) | $1,580 | $1,193 | $387 | $219,842 |

| Month 180 (Year 15) | $1,580 | $878 | $702 | $161,590 |

| Month 240 (Year 20) | $1,580 | $650 | $930 | $119,200 |

| Month 300 (Year 25) | $1,580 | $360 | $1,220 | $65,800 |

| Month 360 (Year 30) | $1,580 | $9 | $1,571 | $0 |

Look at month 1: out of your $1,580 payment, only $226 actually reduced what you owe. That's about 14% of your payment going toward equity. The rest — $1,354 — went straight to the bank as interest.

By month 360, the entire picture is reversed. Nearly the full payment is pure principal. The loan is done.

Over 30 years, you'll have paid a total of about $568,880 on a $250,000 loan. That means you paid approximately $318,880 in interest alone — more than the original loan amount. You essentially bought your house twice.

The math isn't designed to cheat you. It's the natural consequence of borrowing a large amount at interest over a long period. But knowing it means you can make smarter decisions — which is exactly what a mortgage amortization calculator helps you do.

What Is a Mortgage Amortization Schedule?

An amortization schedule is a table that shows every single payment you'll make over the life of your loan. For each month, it breaks down:

- Payment number (month 1, month 2, etc.)

- Total monthly payment

- Amount going to interest

- Amount going to principal

- Remaining loan balance after payment

This table exists for the entire duration of your loan — whether that's 15, 20, or 30 years. It's one of the most powerful documents a homeowner can have, because it shows you exactly where your money is going at every point in time.

Most people never ask for this. But if you did, you'd probably rethink a lot of your mortgage strategy.

Enter your loan details and get a complete month-by-month or year-by-year breakdown instantly. No sign-up needed.

The Front-Loading of Interest: Why It Matters More Than You Think

There's something every homeowner should understand: mortgage lenders structure your payments so that you pay most of the interest in the first half of the loan. This is entirely intentional — and it protects the lender.

If you sell the house or refinance after 7 years, the lender has already collected most of what they planned to earn from you. For you as a borrower, this creates some important realities:

- If you sell in year 5, you've barely touched the principal — you've paid a lot of interest but built relatively little equity beyond your down payment and any appreciation.

- If you refinance, you reset the clock entirely and start paying mostly interest again on a new loan. Your monthly payment may drop, but your total cost can increase significantly.

- The early years are the most expensive. Because the balance is highest early on, that's when each dollar of interest costs the most.

After 5 years of $1,580 payments on a $250,000 loan at 6.5%, you've paid $94,800 total — but your balance has only dropped by about $12,873. The rest ($81,927) was interest. You have about 5% equity built through payments alone (not counting any appreciation).

How Extra Payments Can Transform Your Mortgage

This is the most practical takeaway from understanding amortization: making extra payments toward your principal can save you a staggering amount of money.

Here's why it works. Your interest is calculated each month based on the remaining balance. If you reduce the balance faster by paying extra principal, the interest charged going forward becomes lower. You're not just paying off the loan quicker — you're shrinking the interest that would have been charged on every future payment.

Back to our $250,000 example at 6.5% for 30 years:

| Scenario | Monthly Payment | Loan Paid Off In | Total Interest | Interest Saved |

|---|---|---|---|---|

| No extra payments | $1,580 | 30 years | $318,880 | — |

| +$100/month extra | $1,680 | ~26.5 years | $264,000 | ~$54,880 |

| +$200/month extra | $1,780 | ~24 years | $248,000 | ~$70,880 |

| +$500/month extra | $2,080 | ~19 years | $178,000 | ~$140,880 |

An extra $200 a month saves over $70,000 in interest and pays the loan off 6 years early. That's the power of reducing principal early, when the balance — and therefore the interest charge — is highest.

Practical tips for making extra payments

- Round up your payment. If it's $1,580, pay $1,600. The small rounding adds up significantly over decades.

- Pay bi-weekly instead of monthly. Making 26 half-payments per year equals 13 full payments — one extra per year, with no change in lifestyle.

- Apply windfalls directly to principal. Tax refunds, bonuses, and inheritances make powerful lump-sum payments early in the loan.

- Confirm with your lender that extra payments are being applied to principal, not to future scheduled payments.

Use the Extra Payments tab in our mortgage calculator to see how much time and money you save for your specific loan.

Fixed-Rate vs. Adjustable-Rate Mortgages: How Amortization Differs

Amortization works differently depending on the type of loan you have.

With a fixed-rate loan, a mortgage amortization calculator gives you complete certainty about every payment for the life of the loan. With an ARM, it gives you the baseline scenario — the actual schedule will shift if rates change after the fixed period ends.

15-Year vs. 30-Year Mortgage — What the Numbers Actually Show

This is the question nearly every homebuyer faces. The amortization math tells a very compelling story. Let's compare two scenarios for the same $250,000 loan at 6.5%:

| 30-Year Mortgage | 15-Year Mortgage | |

|---|---|---|

| Monthly Payment | $1,580 | $2,180 |

| Extra Cost Per Month | — | +$600/month |

| Total Interest Paid | ~$318,000 | ~$142,000 |

| Interest Saved | — | $176,000 |

| Loan Paid Off | Year 30 | Year 15 |

| Equity at Year 10 | ~$31,000 | ~$122,000 |

The 15-year mortgage costs $600 more per month — but saves $176,000 in total interest and puts you debt-free 15 years earlier. The equity you build in year 10 is nearly 4× higher.

The 30-year option gives you lower monthly payments and more cash flow flexibility. If you invest the $600 monthly difference at a return higher than your mortgage interest rate, the 30-year can actually come out ahead financially. It depends on your discipline, your investment return assumptions, and how much you value the psychological security of owning your home free and clear.

The 15 vs. 30 decision is highly personal and depends on your income, debts, investment returns, and how long you plan to stay. Our mortgage calculator's Compare tab shows the exact numbers for your specific loan — including total interest, monthly payment, and break-even analysis.

When Does Amortization Matter Most? Key Life Moments

Understanding amortization isn't a one-time exercise. It matters at several key moments in your financial life:

- When you're buying a home: Use a mortgage amortization calculator before you sign anything. Know exactly what you're committing to across different loan amounts, rates, and terms.

- When you're considering refinancing: Refinancing resets your amortization to zero. If you're 10 years into a 30-year mortgage and refinance into a new 30-year loan, you're back to paying mostly interest. Calculate the break-even point before deciding.

- When you're thinking of selling: Check your amortization schedule to see your actual remaining balance and equity before listing the home.

- When interest rates change: A 0.5% difference in rate can mean $40,000–$60,000 over 30 years on a $300,000 loan. Run the numbers anytime rates shift.

- When you receive a windfall: A bonus, tax refund, or inheritance applied to your mortgage early can save more than the same money invested in many scenarios, depending on your rate.

Common Mortgage Amortization Myths — Busted

There's a lot of confusion around this topic. Let's clear it up.

Practical Tips to Apply This Knowledge Today

You now understand how amortization works better than most homeowners. Here's how to put it into action:

- Get your current amortization schedule. Call your lender or check your online account. It should be available at no cost.

- Use a free mortgage amortization calculator. Enter your exact numbers and see where you stand right now — how much equity you have, how much interest is left, and your payoff date.

- Calculate your current equity. Subtract your remaining balance from your home's current market value. That's your actual equity position.

- Explore extra payments. Even $50–$100 extra per month makes a meaningful long-term difference. Use the calculator to see your exact scenario.

- Think before you refinance. Plug the new terms into a mortgage amortization calculator and see the full picture — not just the monthly payment difference.

- Share this with someone buying their first home. Most first-time buyers never see an amortization schedule before signing. This information changes how people think about their mortgage.

Conclusion: Knowledge About Your Mortgage Is Power

Mortgage amortization isn't the most exciting topic in the world. But it's one of the most financially consequential things you can understand as a homeowner.

Once you see how interest front-loading works — how slowly equity builds in the early years, and how dramatically extra payments change your financial future — you stop being a passive bill-payer and start being a strategic homeowner.

A mortgage amortization calculator is free, fast, and gives you the exact numbers you need to take control of your biggest financial commitment. You don't need a financial advisor to run these calculations. You just need five minutes and the willingness to look.

Monthly payment, amortization schedule, extra payment savings, and 15 vs 30 year comparison — all in one tool, formula shown for every result.