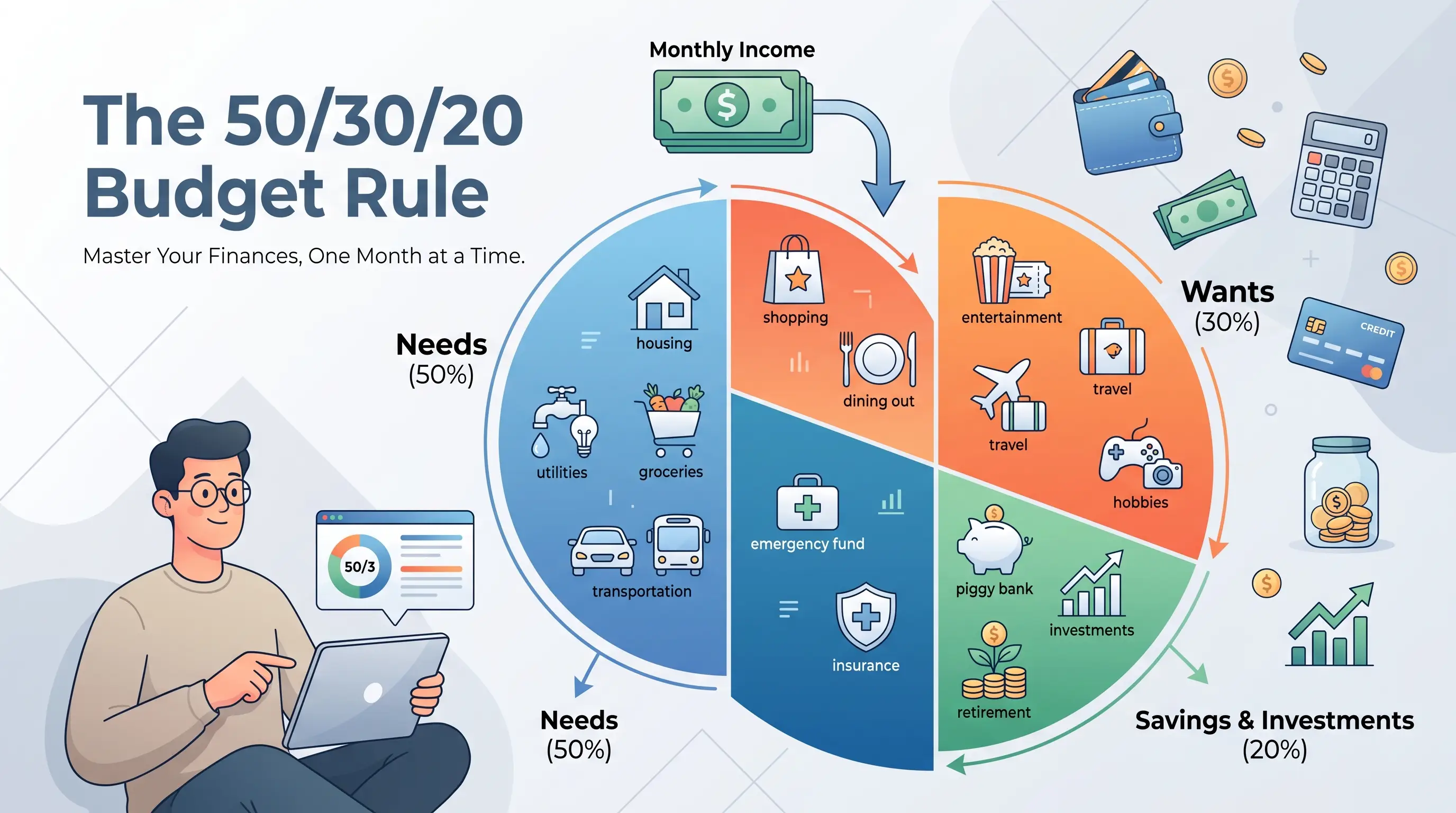

The 50/30/20 rule is the most famous budgeting formula in America — and also the most argued about. Half the internet swears it's the simplest path to financial control; the other half insists it's a relic from 2005 that collapses the moment it meets a modern rent payment. Both sides have a point.

In this guide we'll break down exactly how the rule works, apply it to real U.S. take-home pay at $40,000, $60,000, $80,000, and $100,000 salaries, show where it genuinely breaks in 2026 — and how to adapt it instead of abandoning it.

Want to skip ahead? Enter your own income in our free Budget Calculator and see your three numbers instantly.

What Is the 50/30/20 Rule?

The rule was popularized by Senator Elizabeth Warren — then a Harvard bankruptcy law professor — and her daughter Amelia Warren Tyagi in their 2005 book All Your Worth. It divides your after-tax income into three buckets:

- 50% Needs — things you can't reasonably cancel: rent or mortgage, utilities, groceries, health insurance, minimum debt payments, car payment and gas if you need a car to work.

- 30% Wants — everything that makes life enjoyable but survivable without: dining out, streaming, travel, hobbies, upgraded phone plans, the nicer apartment beyond the basic one.

- 20% Savings & extra debt payoff — emergency fund, retirement contributions beyond any employer match taken pre-tax, investments, and every dollar you pay above minimums on debt.

The genius of the rule is what it doesn't ask you to do: track 47 spending categories. It's a health check with exactly three numbers — coarse enough to maintain, precise enough to expose a problem.

Need vs. Want: The Honest Test

The line people fudge most is needs vs. wants. The test from the original book: a need is something you'd keep paying even if you lost your job tomorrow, because the consequences of stopping are severe.

Groceries are a need; DoorDash is a want. A car payment is a need if you drive to work; the $650/month SUV upgrade over the $350 sedan is $300 of want hiding inside a need. Be ruthless here or the whole exercise lies to you.

Most people discover their "needs" include $200–$400 of disguised wants when they actually audit last month's spending. Premium subscriptions bundled into bills, daily convenience meals, and car upgrades are the most common culprits.

The 50/30/20 Rule on Real U.S. Salaries

The rule uses after-tax (take-home) income. The table below uses approximate take-home figures for a single filer with average state taxes — your exact numbers will vary by state, filing status, and pre-tax deductions, so treat these as ballparks:

| Gross Salary | Approx. Monthly Take-Home | Needs (50%) | Wants (30%) | Savings (20%) |

|---|---|---|---|---|

| $40,000 | $2,750 | $1,375 | $825 | $550 |

| $60,000 | $3,950 | $1,975 | $1,185 | $790 |

| $80,000 | $5,100 | $2,550 | $1,530 | $1,020 |

| $100,000 | $6,150 | $3,075 | $1,845 | $1,230 |

Now the uncomfortable part. That $1,375 needs budget at a $40,000 salary has to cover rent, utilities, groceries, insurance, and transportation. The median U.S. one-bedroom rent alone is hovering around $1,400–$1,500 in 2026 — and far higher in major metros. Which brings us to the real question.

Does the 50/30/20 Rule Still Work in 2026?

Where it works: moderate cost-of-living areas — most of the Midwest and South, smaller metros — and dual-income households, where shared housing costs bring each person's needs percentage down. If your rent or mortgage payment is under about 30% of take-home pay, the classic split is very achievable.

Where it breaks: high-cost cities. In New York, San Francisco, Boston, San Diego, or Seattle, rent alone routinely consumes 40–50% of a single earner's take-home pay, making a 50% total needs cap mathematically impossible without roommates. The rule also strains for anyone with student loans whose minimum payments (a "need") are large, and for single parents carrying childcare costs that can rival rent.

The right response isn't to throw the framework out — it's to change the ratios while keeping the discipline. The three-bucket structure is the value; the exact percentages are a starting point Warren herself described as guidelines, not laws.

Popular Variations and When to Use Them

| Variation | Split | Best For |

|---|---|---|

| 60/30/10 | 60% needs / 30% wants / 10% savings | High-rent cities — keeps you saving something while housing costs are heavy |

| 70/20/10 | 70% needs+debt / 20% wants / 10% savings | Aggressive debt payoff phase or very tight budgets |

| 80/20 | 80% everything / 20% savings first | People who hate categorizing — automate 20% to savings on payday, spend the rest guilt-free |

| 50/40/10 | 50% needs / 40% wants / 10% savings | High earners in LCOL areas who value lifestyle now (use cautiously) |

How to Set Up Your 50/30/20 Budget in 15 Minutes

- 1Find your real take-home pay. Use your actual paycheck deposit, not your salary. If your employer takes 401(k) or health premiums pre-tax, those are already handled — don't double count them.

- 2Run the split. Enter your monthly take-home in our Budget Calculator to get your three targets instantly.

- 3Audit last month against the targets. Pull your last 30 days of bank and card transactions and sort each into needs, wants, or savings. Most people discover their "needs" include $200–$400 of disguised wants.

- 4Fix the biggest gap first. Over on needs? That's a housing/car/insurance problem — one big decision, not thirty small ones. Over on wants? Cap the two worst categories, don't ban everything.

- 5Automate the 20%. Set an automatic transfer to savings for the day after payday. A budget that requires monthly willpower fails; one that runs on autopilot doesn't.

Get your three numbers in 10 seconds

Enter your monthly take-home income and instantly see your 50/30/20 targets — plus adapted splits for your cost of living.

Open Budget CalculatorWhere Should the 20% Actually Go?

Order of operations most financial planners recommend:

- 1A starter emergency fund ($1,000) — so the first car repair doesn't go on a credit card.

- 2Your employer's full 401(k) match — it's a 50–100% instant return with zero market risk.

- 3High-interest debt above ~8% APR. Our guide to the debt snowball vs. avalanche methods breaks down the fastest way to attack it.

- 4A full 3–6 month emergency fund.

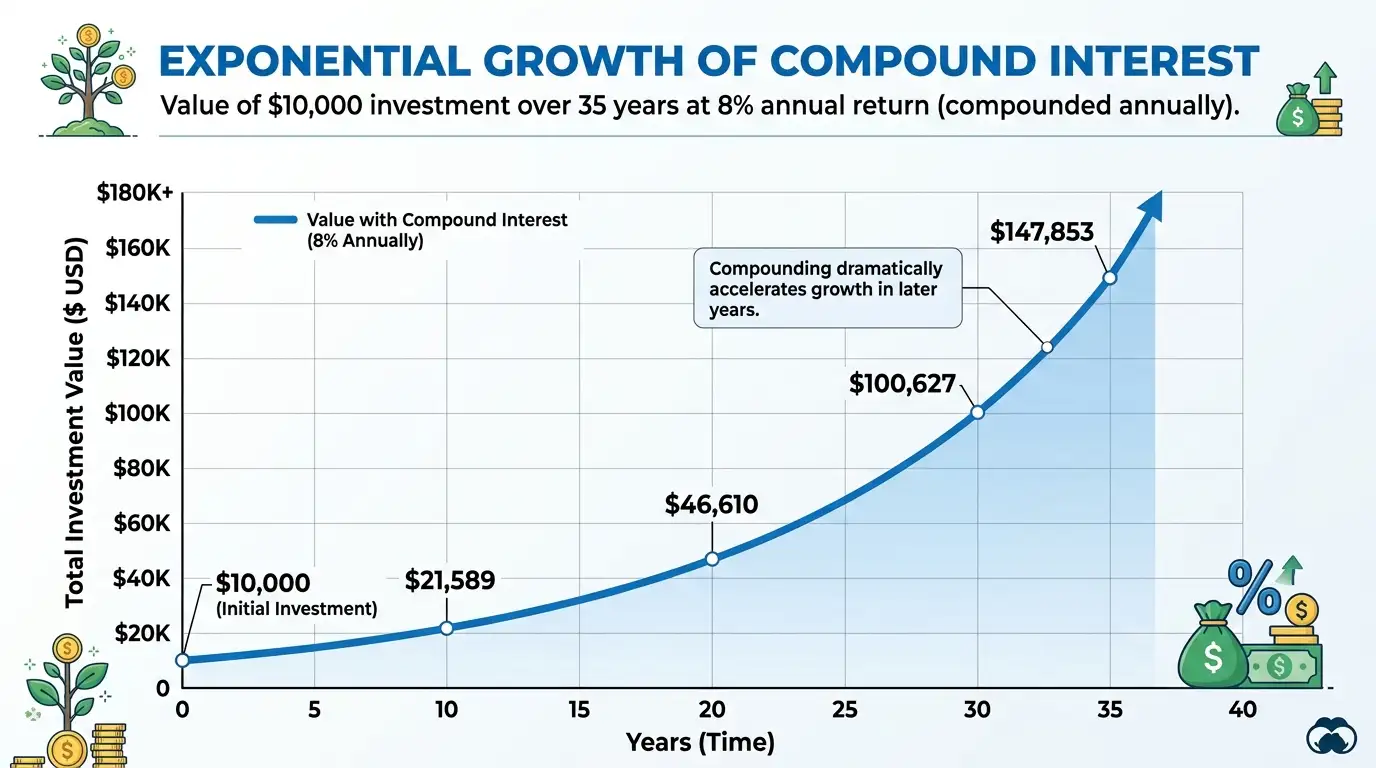

- 5Long-term investing — index funds, Roth IRA, taxable brokerage. Curious what that 20% becomes over decades? See how compound interest grows your money or run it through the Investment Calculator.

The Bottom Line

The 50/30/20 rule isn't sacred math — it's training wheels for financial awareness, and in 2026 it still does that job better than any app with 47 categories. If your city's rent makes 50% impossible, shift to 60/30/10 and keep moving.

The households that build wealth aren't the ones with the perfect ratio; they're the ones that know their three numbers and check them monthly. Get yours in ten seconds with the free Budget Calculator. And if debt is what's eating your "savings" bucket, see how the snowball and avalanche methods can free it up faster than you think. If you want to know how much your 20% turns into after 20 or 30 years, see how much you need to retire.

Frequently Asked Questions

Split your after-tax income three ways: 50% to needs (rent, groceries, utilities, insurance, minimum debt payments), 30% to wants (dining out, entertainment, travel), and 20% to savings and extra debt payoff. It's a simplicity-first budget with just three numbers to track.

Net (after-tax) income — your actual take-home pay. If retirement contributions or health premiums come out of your paycheck pre-tax, work from the amount that hits your bank account and count those pre-tax savings as a bonus on top of the 20%.

In moderate cost-of-living areas, yes. In high-rent metros like NYC or San Francisco, housing alone can consume 40–50% of take-home pay, making the 50% needs cap unrealistic for single earners. The fix is adjusting the ratio — 60/30/10 is a common adaptation — rather than abandoning budgeting altogether.

Minimum payments are needs — missing them has severe consequences. Anything you pay above the minimum counts toward your 20% savings bucket, since it's building your net worth by reducing what you owe.

First, audit for wants hiding inside needs (car upgrades, premium groceries, unused subscriptions bundled into bills). If needs are still over 50%, it's usually a housing or transportation problem — the big fixes are a roommate, refinancing, moving, or a cheaper car, not skipping coffee. Meanwhile, run a 60/30/10 or 70/20/10 split so you keep saving something.

For most people who start by their late 20s or early 30s, saving 15–20% of income consistently (including employer match) is on track for a typical retirement. Starting later requires a higher rate — run your own numbers with our retirement guide to see how much you need.