A $10,000 investment earning 8% per year doesn't grow by $800 every year — it grows by $800 in year one, then $864 in year two, then $933 in year three. The number keeps climbing because each year's gains are themselves earning returns. That is compound interest, and it is the single most important concept in personal finance.

Understanding the maths behind it lets you answer questions that actually matter: How much will $500 a month become in 25 years? Is it better to invest a lump sum now or contribute monthly? At what return rate does my money double in 10 years? What is my investment's CAGR?

This guide works through each calculation type with real formulas and worked examples, so you can verify any projection yourself — or simply hand the numbers to a calculator and know exactly what you're looking at.

CalcMeter's Investment Calculator projects monthly and lump sum returns with a year-by-year breakdown — free, instant, no sign-up.

How Compound Interest Works

Simple interest pays a return only on your original principal. Compound interest pays a return on your principal plus all the interest you have already earned. The longer your time horizon, the larger the gap between the two becomes.

$10,000 invested at 8% compounded annually for 20 years:

A = 10,000 × (1 + 0.08) ^ 20 = 10,000 × 4.661 = $46,610

For most investment accounts — index funds, ETFs, pension accounts — compounding happens continuously as dividends are reinvested and prices appreciate. Using annual compounding (n = 1) is the standard simplification for planning purposes.

"Compound interest is the eighth wonder of the world. He who understands it, earns it. He who doesn't, pays it." — attributed to Albert Einstein

Simple vs. compound: the real difference over time

| Year | Simple Interest (8%) | Compound Interest (8%) | Difference |

|---|---|---|---|

| 1 | $10,800 | $10,800 | $0 |

| 5 | $14,000 | $14,693 | +$693 |

| 10 | $18,000 | $21,589 | +$3,589 |

| 20 | $26,000 | $46,610 | +$20,610 |

| 30 | $34,000 | $100,627 | +$66,627 |

Starting amount: $10,000. By year 30, compound interest produces three times the result of simple interest — entirely from returns earning their own returns.

Calculating Monthly Investment Returns

Most people don't invest a lump sum — they invest a fixed amount each month from their salary. This is called an annuity in financial maths, and it has its own formula: the future value of a recurring payment.

Investing $500/month at 8% annual return for 25 years:

r = 0.08 ÷ 12 = 0.006667 | n = 25 × 12 = 300 months

FV = 500 × [((1.006667)^300 − 1) / 0.006667]

FV = 500 × [7.245 / 0.006667] = 500 × 472.3 = $472,300

You contributed $150,000 over 25 years ($500 × 300 months). The remaining $322,300 is pure investment return — more than double your total contribution — generated entirely by compound growth.

Monthly investing: how much does time matter?

| Monthly amount | Years invested | Total contributed | Final value (8%) | Return earned |

|---|---|---|---|---|

| $500/month | 10 years | $60,000 | $91,473 | $31,473 |

| $500/month | 20 years | $120,000 | $294,510 | $174,510 |

| $500/month | 30 years | $180,000 | $745,180 | $565,180 |

| $1,000/month | 20 years | $240,000 | $589,020 | $349,020 |

| $1,000/month | 30 years | $360,000 | $1,490,359 | $1,130,359 |

$500/month for 30 years ($745K) outperforms $1,000/month for 20 years ($589K) — even though the 30-year investor contributed less money in total ($180K vs $240K). Starting earlier is more powerful than contributing more.

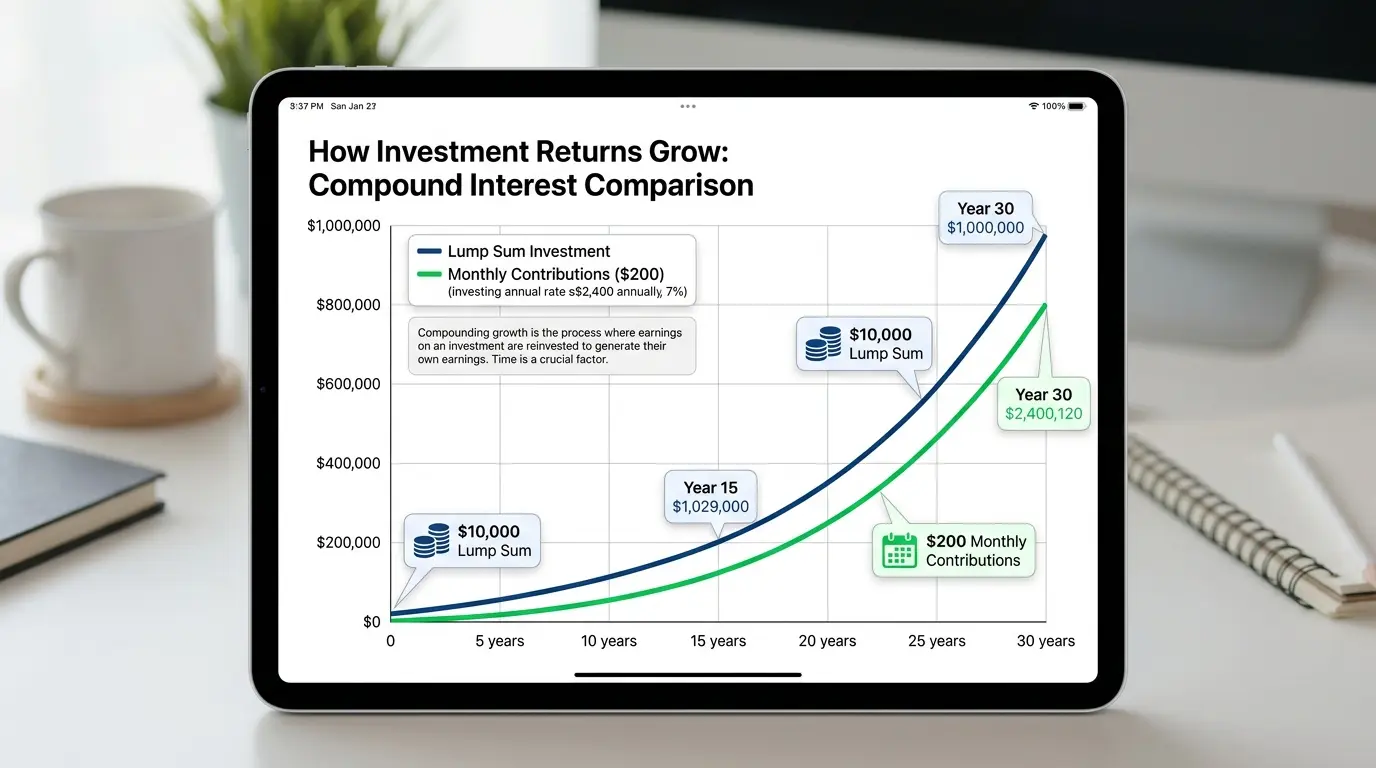

Lump Sum vs. Monthly Investing: Which Grows More?

This is one of the most searched investment questions, and the answer is more nuanced than most articles admit.

When lump sum wins

Research by Vanguard analysed 10-year rolling periods across US, UK, and Australian markets and found that lump sum investing outperformed monthly investing about two-thirds of the time. The logic is straightforward: if markets trend upward over time, investing everything immediately puts more money to work compounding from day one.

Lump sum advantage: $93,219 − $49,085 = $44,134 more

When monthly investing makes more sense

For most people, the lump sum option doesn't exist — you receive income monthly and invest what you can afford. Beyond practicality, monthly investing has a genuine advantage: dollar-cost averaging. By investing the same amount each month regardless of market conditions, you automatically buy more units when prices are low and fewer when prices are high. This smooths your average cost per unit over time.

Monthly investors also experience smaller portfolio swings. In a market downturn, a lump sum portfolio might fall 35% while a monthly investor's equivalent portfolio (with contributions still buying at low prices) might fall only 22%.

If you have a lump sum available and a long time horizon, investing it immediately typically produces higher returns. If you are investing from regular income — which applies to most people — monthly contributions with a consistent schedule is the right approach. Both are far better than not investing.

What Is a Realistic Investment Return Rate?

Every investment projection requires an assumed return rate. Choosing a realistic rate is more important than choosing the right formula. Here is what the historical data shows:

| Investment type | Historical avg. return | After inflation (~3%) | Use for planning |

|---|---|---|---|

| S&P 500 / broad index funds | ~10% per year | ~7% | Yes |

| Diversified stock portfolio | 7–9% | 4–6% | Yes |

| Balanced fund (60% stocks / 40% bonds) | 6–7% | 3–4% | Conservative |

| Bond funds / fixed income | 3–5% | 0–2% | Conservative |

| High-yield savings / cash | 3–5% | Near 0% | Short-term only |

For long-term planning, use 7% (inflation-adjusted) as your base case and run optimistic (10%) and pessimistic (5%) scenarios alongside it. This gives you a realistic range rather than a single number that may or may not materialise.

Historical return rates are the best tool we have for planning, but they are not promises. Market returns vary year to year, and a 10% average includes years of −30% and years of +30%. The averages only materialise reliably over very long periods (15+ years).

What Is CAGR and How Do You Calculate It?

CAGR — Compound Annual Growth Rate — is the single rate of return that would take an investment from its starting value to its ending value over a set number of years, as if it grew at a perfectly steady pace each year.

It is useful because it strips out the year-to-year volatility and gives you one clean number to compare investments, measure fund performance, or verify a projection.

CAGR = (9,000 ÷ 5,000) ^ (1/6) − 1

= 1.8 ^ 0.1667 − 1 = 1.1027 − 1 = 10.27% per year

A fund grew from $10,000 to $18,500 in 8 years:

CAGR = (18,500 ÷ 10,000) ^ (1/8) − 1 = 1.85 ^ 0.125 − 1 = 7.95% per year

Why CAGR is more useful than average return

An investment that gains 50% one year and loses 30% the next has an average return of 10% — but your actual balance is lower than when you started. CAGR avoids this problem because it is calculated from actual start and end values, not an arithmetic mean. Always use CAGR when evaluating real performance.

The Rule of 72: How Long to Double Your Money

The Rule of 72 is the most useful mental maths shortcut in investing. Divide 72 by your expected annual return rate to estimate how many years it takes to double your money.

The Rule of 72 is accurate for return rates between 5% and 12% — the range most long-term investors operate in. Beyond that range, a proper calculation is more reliable.

Dollar-Cost Averaging: Why Monthly Investing Works

Dollar-cost averaging (DCA) is the practice of investing a fixed amount at regular intervals regardless of what the market is doing. It is the mechanism behind every monthly investment plan — pension contributions, recurring ETF purchases, or automated transfers into an index fund.

How DCA reduces your average cost per unit

| Month | Investment | Unit price | Units bought |

|---|---|---|---|

| January | $500 | $50.00 | 10.0 |

| February | $500 | $40.00 | 12.5 |

| March | $500 | $45.00 | 11.1 |

| April | $500 | $55.00 | 9.1 |

| Total | $2,000 | Average: $47.50 | 42.7 units |

Your average cost per unit: $2,000 ÷ 42.7 = $46.84. If you had invested $2,000 as a lump sum in January at $50/unit, you would have bought only 40 units — and your cost per unit would be $50. DCA bought you 2.7 more units at a lower average price, purely by spreading the investment across months.

DCA doesn't always win — if prices only go up, you would have been better off investing everything on day one. But it removes the biggest behavioural risk in investing: trying to time the market and failing.

Enter your monthly amount, return rate, and years — get a full year-by-year breakdown of how your investment grows.

How Much to Invest Monthly to Reach Your Goal

Working backwards from a target amount is often more useful than projecting forward. Here is what you need to invest monthly at 8% annual return to reach common milestones:

| Target | In 10 years | In 20 years | In 30 years |

|---|---|---|---|

| $100,000 | $546/month | $170/month | $67/month |

| $250,000 | $1,364/month | $425/month | $168/month |

| $500,000 | $2,728/month | $849/month | $335/month |

| $1,000,000 | $5,466/month | $1,698/month | $671/month |

The numbers in the 30-year column are a fraction of the 10-year column — same destination, dramatically lower monthly cost. Time is the variable most under-appreciated by people who delay starting.

5 Common Investment Calculation Mistakes

- Using nominal returns instead of real (inflation-adjusted) returns. A 10% return when inflation is 3% is really 7% in purchasing power. Always think in real returns when planning long-term goals like retirement.

- Ignoring fees. A 1% annual fund management fee sounds small, but over 30 years it can consume 20–25% of your total portfolio value. Always calculate returns net of fees.

- Assuming a constant return rate. Markets don't deliver 8% every year — they deliver −30% some years and +25% others. The average smooths out, but sequence of returns matters, especially near retirement.

- Calculating CAGR as an average instead of a geometric rate. Adding up annual returns and dividing by years gives you the arithmetic mean, not CAGR. An investment that gains 50% then loses 50% has an arithmetic average of 0% — but you have actually lost 25% of your money.

- Not accounting for taxes. Capital gains taxes, dividend taxes, and withdrawal taxes can significantly reduce your actual returns. Tax-advantaged accounts (ISAs, 401(k)s, pension funds) shelter your gains — always max these before investing in taxable accounts.

Frequently Asked Questions

The Bottom Line

Investment returns are not magic — they are the output of a small number of variables: how much you invest, how often, at what rate, and for how long. The formula is the same whether you are projecting a lump sum or a monthly contribution; compound interest does the heavy lifting in both cases.

The single most powerful insight from the maths is how dramatically time affects the outcome. Not starting because you can only invest a small amount is almost always the wrong call — a modest monthly contribution over 25 years outperforms a large contribution over 10 years, every time.

Use a realistic return rate (7% after inflation for index fund investors is the widely accepted benchmark), account for fees and taxes, and let compounding do the rest. The calculator does the arithmetic — your job is to stay invested long enough for the numbers to work.

CalcMeter's free Investment Calculator shows your full growth breakdown with CAGR. No sign-up, no paywalls.