Every year, as Ramadan approaches, millions of Muslims open their phones and search for the same thing: "how to calculate zakat." The obligation is clear — 2.5% of your eligible wealth — but the questions pile up fast. Which assets count? What's the nisab this year? Can I subtract my debts? What about my investments? My gold jewellery? My retirement account?

The answers aren't complicated once you understand the underlying framework. Zakat has three building blocks — the nisab threshold, the hawl condition, and the 2.5% rate — and once you see how they fit together, every asset type becomes a straightforward calculation.

This guide covers all of it: who must pay, what's zakatable, what isn't, how to handle debts, and worked examples for every major asset class.

CalcMeter's free Zakat Calculator handles cash, gold, investments, and business assets — with your total calculated instantly.

What Is Zakat and Who Must Pay It?

Zakat (زكاة) is the obligatory annual almsgiving that is the third pillar of Islam. The word literally means "purification" — the idea being that giving away a portion of your wealth purifies the rest of it and fulfils a social obligation to those in need.

Zakat is not charity in the voluntary sense. It is a religious duty, and for those who meet the conditions, it is as obligatory as the five daily prayers.

The four conditions for zakat to be obligatory

- Muslim — Zakat is only obligatory upon Muslims.

- Adult & sane — A minor or a person who is mentally incapacitated is not liable.

- Ownership of nisab — Your net zakatable wealth must meet or exceed the minimum threshold (nisab).

- Hawl — You must have held that wealth above the nisab for a full lunar year (approximately 354 days).

This guide covers Zakat al-Mal — the annual wealth tax. Zakat al-Fitr is a separate, smaller obligation paid at the end of Ramadan (typically a fixed food amount per household member) and is calculated differently.

Understanding Nisab: The Minimum Wealth Threshold

The nisab is the minimum amount of wealth you must possess before zakat becomes obligatory on you. Think of it as the tax-free threshold — if your net zakatable assets fall below this level, you owe nothing.

Nisab is defined by the Prophet Muhammad ﷺ in terms of gold and silver, and there are two separate nisab standards:

| Standard | Weight | Traditional unit | Use |

|---|---|---|---|

| Gold Nisab | 87.48 grams | 7.5 tola | Used when calculating zakat on gold holdings |

| Silver Nisab | 612.36 grams | 52.5 tola | Recommended for cash, savings, and mixed assets |

Gold nisab vs. silver nisab — which should you use?

Because gold and silver prices fluctuate daily, the cash equivalent of each nisab changes constantly. As of 2026, the gold nisab converts to a significantly higher cash value than the silver nisab. Most contemporary scholars — and major zakat organisations like Islamic Relief, Muslim Aid, and Zakat Foundation of America — recommend using the silver nisab for cash and mixed assets, because:

- It is the lower threshold, meaning more Muslims meet the obligation.

- It channels more wealth to those who need it.

- It is consistent with the broader intent of zakat as a tool of social welfare.

To find today's nisab in your currency, multiply the current silver spot price per gram by 612.36. Use CalcMeter's Zakat Calculator for the live value, or check a trusted Islamic financial resource for the updated nisab in your local currency.

"If your net zakatable wealth has been above the nisab for a full lunar year, 2.5% of it belongs to those in need. The calculation is one of Islam's most precisely defined financial obligations."

What Is the Hawl? The Lunar Year Condition Explained

The hawl (حول) is the Islamic lunar year — approximately 354 days — during which your wealth must continuously meet or exceed the nisab before zakat becomes due.

Practically, this works as follows: the day your wealth first reaches the nisab, your hawl clock starts. On the same Islamic date the following year, if your wealth is still at or above the nisab, you calculate and pay zakat on whatever you hold at that point.

Key hawl rules to know

- You don't need to hold the same money for 12 months. Your wealth just needs to stay at or above the nisab throughout. If it dips below and then recovers, the hawl resets from the recovery date.

- Calculation is a snapshot, not an average. You calculate zakat based on what you own on your hawl anniversary — not an average of the year's balance.

- Your hawl date is personal. Many Muslims choose to calculate on the 1st of Ramadan for convenience, but your actual hawl is tied to when you first reached the nisab.

- Newly acquired wealth. Assets you acquire mid-year that become part of your main zakatable wealth pool are typically included in your existing hawl. Assets acquired close to your hawl date may need separate tracking — consult a scholar for complex cases.

Pick an Islamic date that's easy to remember — the first of Ramadan is a popular choice — and calculate your zakat on that date each year. As long as your wealth was consistently above nisab throughout, this is a valid and widely followed approach.

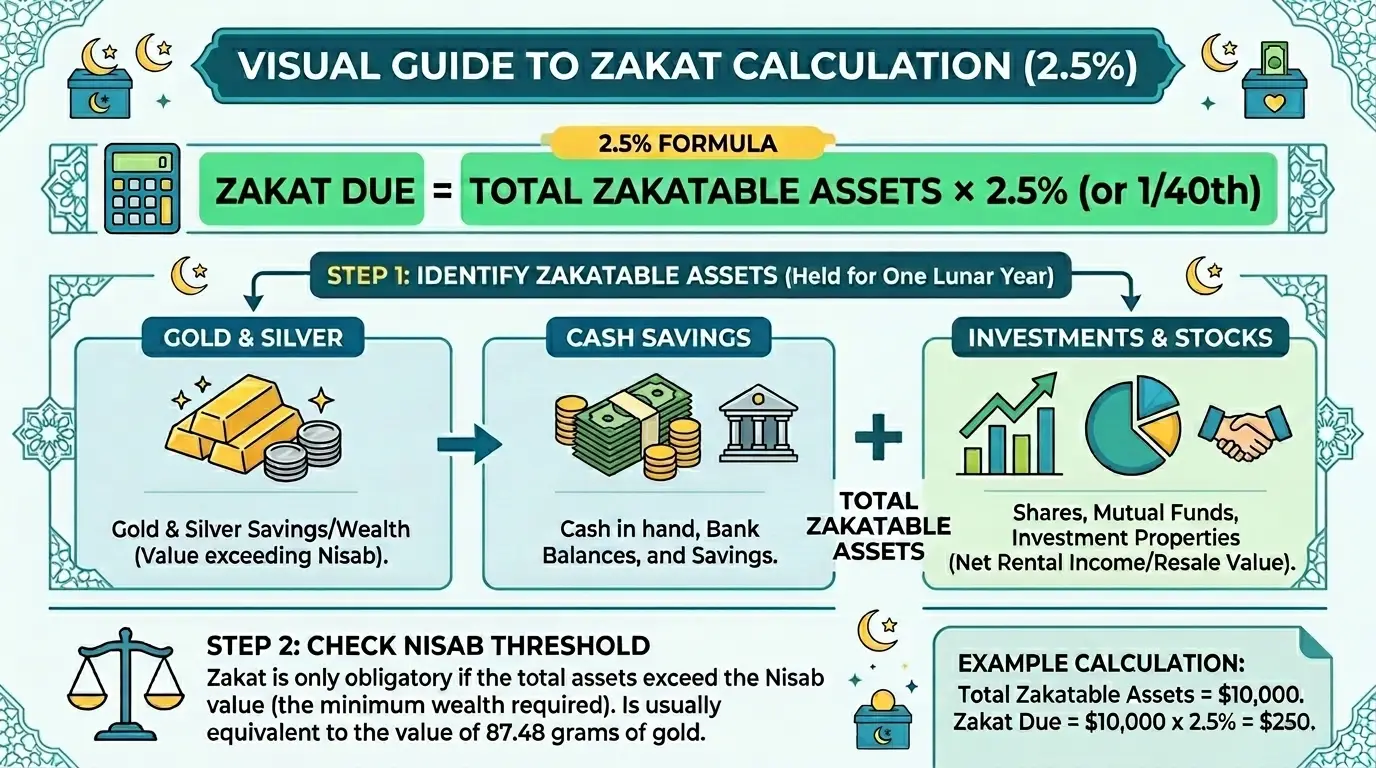

The Zakat Formula: How 2.5% Works

Once you've confirmed you meet the nisab and hawl conditions, the calculation itself is straightforward:

e.g. You hold $40,000 in savings, $5,000 in gold, $10,000 in investments, and owe $3,000 in bills due this month:

Net Wealth = ($40,000 + $5,000 + $10,000) − $3,000 = $52,000

Zakat Due = $52,000 × 0.025 = $1,300

The 2.5% rate (1/40th of wealth) is fixed by the Sunnah and applies to all standard zakatable assets — cash, savings, gold, silver, business inventory, and most investments. Agricultural and mineral assets have different rates, but these are rarely relevant for most Muslims calculating personal zakat.

Step-by-Step: How to Calculate Your Zakat

Follow these six steps every year on your hawl date:

- 1 List all your zakatable assets — cash, bank balances, gold, silver, business stock, receivables owed to you, and investments.

- 2 Value each asset at its current market value on your hawl date.

- 3 List your short-term liabilities — debts, bills, and obligations due within the current lunar year.

- 4 Subtract liabilities from assets to get your net zakatable wealth.

- 5 Check against the nisab — if your net wealth exceeds the nisab, zakat is due.

- 6 Multiply by 2.5% — this is what you owe.

Enter your assets across cash, gold, and investments — CalcMeter computes your total zakat amount instantly.

Zakat on Cash & Bank Savings

Cash is the simplest zakatable asset. All cash you own — whether in a current account, savings account, fixed deposit, or held as physical notes — is fully zakatable if it has been above the nisab for a full hawl.

Total = $27,000

Zakat = $27,000 × 0.025 = $675

What counts as "cash"?

- Current and savings account balances

- Fixed deposits and term accounts (include the full balance)

- Physical cash (notes and coins)

- Money in digital wallets, PayPal, or similar platforms

- Money owed to you that you are reasonably confident of receiving

Zakat is calculated on savings held for a full lunar year, not on your monthly salary as it comes in. Your salary is only zakatable once it has sat in your account long enough to become part of your accumulated savings above the nisab on your hawl date.

Zakat on Gold & Silver

Gold and silver are the original currencies of zakat. Both are fully zakatable if they exceed the nisab and have been held for a hawl.

Value = 120 × $95 = $11,400

Zakat = $11,400 × 0.025 = $285

Adjusting for purity

Gold is rarely 100% pure. Adjust the weight for karat purity before applying the formula:

| Karat | Purity | Multiplier | Example: 100g of this gold |

|---|---|---|---|

| 24K | 99.9% | × 1.000 | 100g of pure gold |

| 22K | 91.7% | × 0.917 | 91.7g of pure gold |

| 21K | 87.5% | × 0.875 | 87.5g of pure gold |

| 18K | 75.0% | × 0.750 | 75.0g of pure gold |

Is gold jewellery zakatable?

This is the most debated question in zakat on gold. Here is where the four major schools stand:

- Hanafi: All gold and silver is zakatable regardless of use, including jewellery worn regularly.

- Shafi'i, Maliki, Hanbali: Gold jewellery used for personal adornment (not for investment or hoarding) is generally exempt.

If you follow the Hanafi school or prefer the more cautious approach, include all gold jewellery in your zakat calculation. If you follow the majority position, you may exclude jewellery worn for personal use. Consult a qualified Islamic scholar if you are unsure which ruling applies to you.

Zakat on Investments, Stocks & Mutual Funds

Modern investment vehicles did not exist in the classical age of Islamic jurisprudence, so scholars have developed rulings based on the underlying nature of each asset. The key question is: what is your intent — short-term trading or long-term wealth building?

Stocks: trading intent vs. long-term holding

| Intent | How to calculate zakat | Example |

|---|---|---|

| Short-term trading (frequent buying and selling) | 2.5% of total portfolio market value on hawl date | Portfolio worth $30,000 → Zakat = $750 |

| Long-term investment (holding shares in a company) | 2.5% of your proportional share of the company's zakatable assets (cash, receivables, inventory) | More complex — use a zakat calculator or consult a scholar |

For most individual investors who buy and hold index funds or ETFs for retirement or long-term growth, the simplified approach is to calculate 2.5% of the current market value of your portfolio — this is the conservative position most scholars recommend for its practicality.

Mutual funds and SIPs

For money-market funds, liquid funds, and short-term bond funds: calculate 2.5% of the current NAV (net asset value) of your holdings on your hawl date. For equity mutual funds (including SIP investments in index funds), the same logic as long-term stocks applies — most scholars accept 2.5% of current market value as a valid approach.

Zakat = $18,500 × 0.025 = $462.50

Zakat on Business Assets

If you own a business, zakat applies to the business's liquid zakatable assets — not the business as a whole. Fixed assets like machinery, property, and equipment are generally exempt. What is zakatable:

- Business cash and bank balances — fully zakatable at 2.5%

- Stock/inventory held for sale — valued at current market value, zakatable at 2.5%

- Trade receivables (debts owed to your business) — include the amounts you are reasonably confident of collecting

Net = ($15,000 + $20,000 + $5,000) − $8,000 = $32,000

Zakat = $32,000 × 0.025 = $800

Rental property

The property itself (the fixed asset) is not zakatable — bricks and mortar are not liquid wealth. However, net rental income you have accumulated and held above the nisab for a hawl is zakatable at 2.5%. Deduct legitimate expenses (maintenance, mortgage payments, taxes) before calculating zakat on the income.

What Is NOT Zakatable — Assets to Exclude

Many assets people worry about are actually exempt from zakat. The rule of thumb: assets held for personal use and non-liquid fixed assets are generally not zakatable.

How to Deduct Debts & Liabilities

You are permitted to subtract certain liabilities from your total zakatable assets before applying the 2.5% rate. The key rule: only deduct debts that are currently due within the lunar year.

| Liability type | Deductible? | How much to deduct |

|---|---|---|

| Credit card balance due | Yes | Full amount currently owed |

| Bills due this month | Yes | Full amount |

| Current mortgage instalment | Yes | Only the current payment due — not the entire balance |

| Total remaining mortgage balance | No | Long-term debt not deductible in full |

| Student loan total outstanding | No | Only the current year's repayments are deductible |

| Personal loan repayments due this year | Partial | Amount due within the current hawl year |

A common mistake is subtracting the entire outstanding mortgage balance from zakatable wealth. Only the payments currently due (this month's or this year's instalments) are deductible. The remainder is a long-term liability and is not deducted from your zakat base.

A Complete Worked Example

Let's walk through a realistic zakat calculation for a working professional:

| Asset / Liability | Value | Zakatable? |

|---|---|---|

| Savings account balance | $32,000 | Yes |

| Cash at home | $800 | Yes |

| Gold jewellery (200g @ $95/g, 22K) — Hanafi | $17,423 (200 × 0.917 × $95) | Yes |

| Investment portfolio (stocks) | $12,000 | Yes |

| Personal car | $18,000 | No |

| Primary home | $350,000 | No |

| Credit card bill due this month | −$1,500 | Deduct |

| Mortgage payment due this month | −$1,200 | Deduct |

5 Common Zakat Calculation Mistakes

- Deducting the entire mortgage balance. Only current payments due are deductible — not the full outstanding loan. This is the most common error and leads to significantly understated zakat.

- Forgetting receivables. Money owed to you by others — loans you have made, unpaid invoices — is zakatable wealth. If you expect to collect it, include it.

- Using the gold nisab for cash savings. Most scholars recommend the silver nisab for cash and mixed assets. Using the gold standard incorrectly exempts a large amount of wealth from zakat.

- Miscalculating gold karat purity. Zakat on gold is based on the weight of pure gold content, not the total weight of the piece. A 200g 22K gold necklace contains only 183.4g of pure gold.

- Paying zakat on gross assets instead of net. Always subtract your short-term liabilities before applying the 2.5% rate. Paying on gross wealth overstates your zakat obligation.

Frequently Asked Questions

The Bottom Line

Zakat is one of Islam's most precisely defined financial obligations, and calculating it correctly is an act of worship in itself. The framework is consistent: identify your zakatable assets, subtract short-term liabilities, check against the nisab, and pay 2.5% of whatever remains if you've held it for a full lunar year.

The details — which assets to include, how to value gold, how to handle investments — can feel complex at first, but they follow logical principles once you understand the intent: liquid wealth that you hold and do not need for personal survival belongs partly to those in need.

If you have complex assets — a business, multiple investment accounts, international holdings, or significant debts — it is worth consulting a qualified Islamic scholar or a specialist in Islamic finance to ensure your calculation is accurate. For the majority of Muslims, however, the framework above covers everything needed to calculate zakat correctly.

CalcMeter's Zakat Calculator covers cash, gold, investments, and business assets. No sign-up. No paywalls.